Due to extreme demand, almost all states have extended their deadlines to sign up for health insurance for January 2017.

Connecticut and New York: Saturday the 17th (tomorrow)

California and all 40 states that use Healthcare.gov: Monday Dec 19

Massachusetts, Rhode Island and Washington: Friday Dec 23

Colorado did not officially extend their deadline, but posted this note: If you were unable to complete your enrollment by Thursday (12/15) and need coverage on Jan 1st, please call our Customer Service Center at 855-752-6749 before you complete your enrollment.

No, she lived in Indiana in 2013. In Dec 2013, she signed up for 2014 coverage thru the federal website (since Indiana refused to create their own state exchange), so she was covered federally as a resident of Indiana for the first part of the year. In June 2014, she moved to Washington and signed up for coverage there through the WA state exchange; that coverage started on July 1. She also cancelled her federal coverage effective June 30. There was no gap. It was a hassle; the change-of-circumstance application was a new thing at the time. The exchange people kept giving us conflicting information about what would constitute proof of residency in Washington. The application kept getting stuck in their process because no one knew what to do with it. But they did get it done, finally.

Before ACA, if you moved to another state, you had to hope you could get coverage in the new state and if you couldn’t, you were SOL. Now you can live your life, move after college if that’s what you want to do, and still know that you’ll have insurance.

What caught my attention in calmom’s post was this:

… which seems to be describing my D’s situation. I’m certain calmom didn’t mean that my D should have been without insurance for 6 months just because she moved. So I wanted to get clarification.

No, I didn’t mean that your DD should have gone without insurance. I just meant that its also possible for a young person who has chosen to go without insurance to decide that if they get injured or sick, they can always just quit their job or move. A move from Indiana to Washington isn’t the sort of thing someone does on a whim, but in states like California it can be a move across county lines. I think it’s especially true for younger people - the same demographic that the companies need to sign up - because they tend to be more mobile.

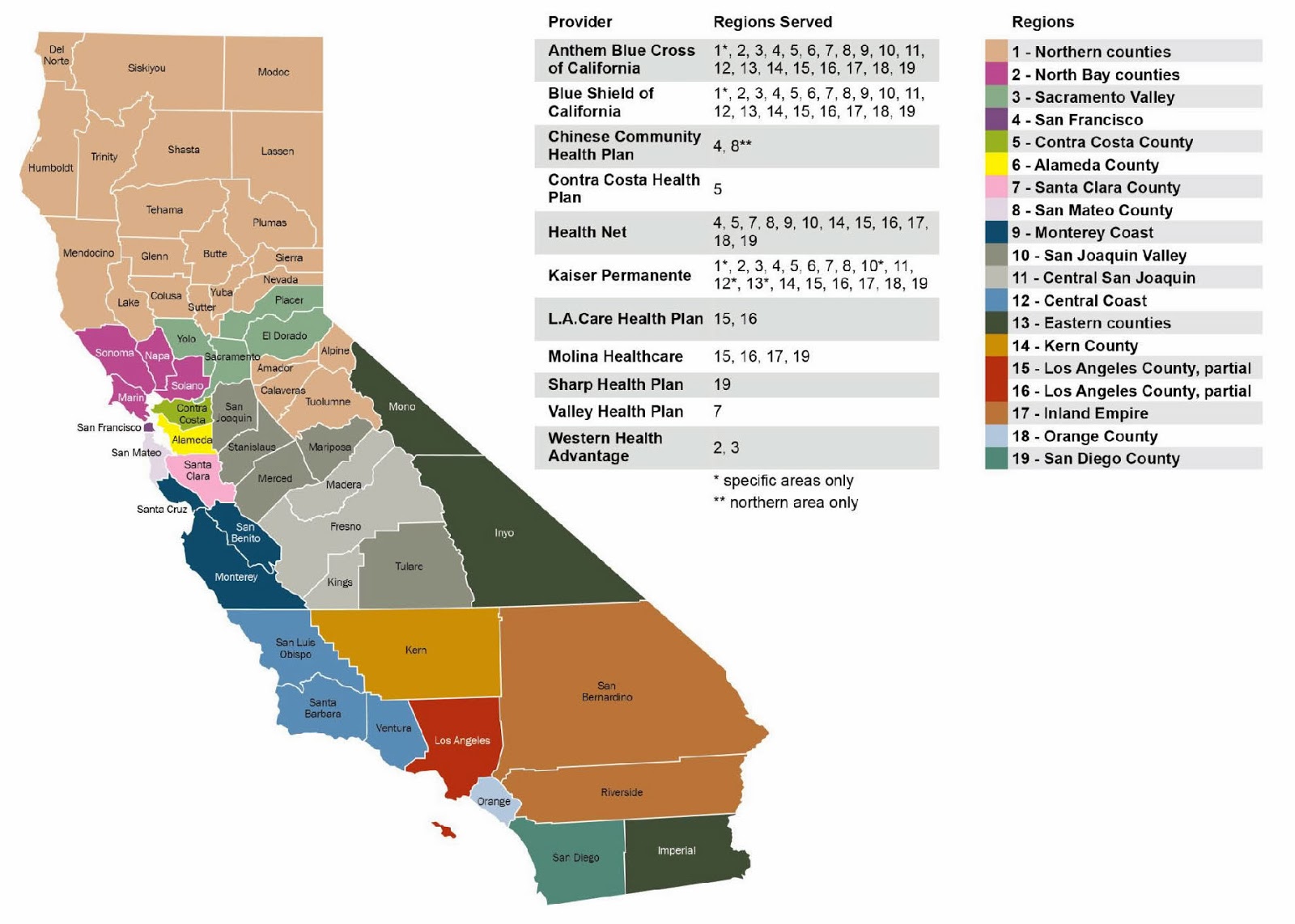

My view is probably colored by living an an urban/suburban area of California that has 19 different regions, with some that are particularly small geographically in the SF bay area - see http://2.bp.blogspot.com/-mJHH1xlks_o/Uo5xJt90JoI/AAAAAAAAAM4/Kk7MFQQGTt0/s1600/table_Page_7.jpg – There’s a lot of movement among San Francisco, Marin, San Mateo, Santa Clara, Alameda & Contra Costa counties as it is, even without a desire to qualify to change health plans mid year. (Another downside of ACA is that it also impedes mobility, if moving a short distance away across a county line means that an already-insured person needs to give up access to a network provider.).

Thanks, calmom, I knew you didn’t want my D to be uncovered. It is a pain in the neck sometimes. All the problems you mention could be. … well, you know.

Right, @calmom, but we now know that you can’t move to a new region and get new insurance if you weren’t previously insured, as of July. That’s a good rule change! I wish it had gotten more publicity.

Yes – I wasn’t aware of the rule change. Fortunately, in post #951 – I used past tense to discuss that-- “One of the big flaws …was that anyone could…” …so my point still stands even though I didn’t footnote it with what I didn’t yet know (that things changed in July, suggesting that I’m not the only one who considered the previous looseness of the changed-circumstance process to be a flaw). My point being that people may be signing up this year vs. past years because they are more concerned about their ability to sign up later on.

If information about hat rule change was widely understood, that could be a factor driving enrollment notwithstanding the election results, but I’m guessing that most people don’t really have a detailed knowledge, and it’s more of a factor of now being fearful of losing something that was previously taken for granted.

Procrastination is a factor, but these huge numbers are being driven by fear IMO. Or the mistaken belief that ACA plans will somehow be grandfathered in.

The ironic thing is that I’d bet that if you look at this year’s new enrollments alone, they’re likely people who don’t use that much in health services compared to people who’ve been enrolled all along (or presumably they would have enrolled much sooner). They’re the people who needed to enroll in the first place to make the whole thing profitable for insurers. They won’t be able to save themselves, since they waited until it was too late, but they will prove the point that if we had had a stronger penalty or other incentive for healthier people to enroll, ACA would have been the success it needed to be.

I wonder if some of it is driven by wanting to squeeze in medical care in the next few months - that knee operation they’ve been putting off, that IUD, etc…

Maybe the penalty isn’t very high for those with lower incomes? The penalty is something not to ignore for us. Well, we’re not going to go without health insurance.

There is a penalty exemption if your premiums based on a Silver plan would be more than 8.13% of your income. There are also exemptions if you were a victim of domestic violence, if you had expenses caring for a sick or elderly family member or if some family member died. There are other exemptions also. (Illegal alien, member of an Indian tribe, member of a health sharing ministry and others).

Midwest, the penalty is negligible. ACA assumes that people are smart and will jump at the chance for guaranteed coverage. Lesson learned; people aren’t smart. They have to be coerced.

It hasn’t been that simple to navigate. Look at the issues some of us had, making our own right decisions. Including thumper, who started this thread. It’s not just signing up, picking A, B…E, F. You deal with doc availability, whether your local hospital goes off net, projecting contingencies, and cost differences, etc. Hard enough for those of us who understand the variables.

Some Bronze plans startle me. You’re asked to pay premiums and, in some cases, thousands of $, before large reimbursements come in. To my mind, that both discourages choosing a plan…and getting med services. Even some Silver are out of whack.

“Some Bronze plans startle me. You’re asked to pay premiums and, in some cases, thousands of $, before large reimbursements come in. To my mind, that both discourages choosing a plan…and getting med services. Even some Silver are out of whack.”

It is complicated. Because even the more “generous” plans (gold, platinum) can cost so much that you might be better off no matter what buying the lower metal plan, at least in the offerings in my state. The maximum out of pocket kicks in at a certain level and sometimes it is less than the difference in premiums between a bronze and a gold. Given health care costs, it doesn’t take much to reach that max out of pocket if you have one or two things that need attention and different testing.

It is a pain in the neck sometimes. All the problems you mention could be. … well, you know.

It is a pain in the neck sometimes. All the problems you mention could be. … well, you know.{kind=link}