But a 10% investment outside of Roth will be subject to capital gains at 15-20% when realized. No tax on a Roth.

Super simple example, 10K invested that gets a compounded 10% return after 40 years = 452.6k

Cap gains = 442.6k

Even using a 15% rate, that will cost you 66.4k. 20% will cost you 88.5k

Well given the title of this thread, I don’t know why we are arguing Roths. The question was what to do after they funded their Roth. I have been suggesting investing it in non-retirement accounts, since others were advocating additional retirement vehicles (like SEP IRA or solo 401k).

The only reason I spoke about Roths is because it sounded like you didn’t understand that you and your daughter actually are able do a Roth, especially if the only reason you weren’t was because of income limits.

Sure, saving is the first necessary step. But once a young person has committed to that, a proper long term financial plan will focus on asset allocation, diversification, minimizing fees/costs, and minimizing or optimizing taxes.

Retirement accounts are key to that last bit, assuming of course that the funds being saved are intended for retirement.

Unless there is a planned use of funds in the short term (buying a house or building an emergency fund), most young people will be best served long term by plowing as much into retirement accounts as they can. There just isn’t a compelling case for taxable long term savings until retirement accounts have been maxed.

In practice, most youngsters might need to decide how to balance saving for short term priorities such as buying a house vs longer term priorities.

Have him check to see if he can save after tax money into his 401k. Most tech companies allow this. Once it’s in the 401k, again, if his company allows it, and most do, he can convert it to a Roth, hence “backdoor.”

So why do this as opposed to just saving in a taxable account since you pay income tax on the money going in? Roth money compounds and withdraws tax free, isn’t subjected to RMDs and passes to heirs tax free.

The 401k, including all pretax, post tax and matching can be almost $70k. Doing that, and then converting, is technically called a mega backdoor Roth. A regular backdoor comes from an IRA.

Solo 401k and SEP IRA support both pre-tax (traditional) and after-tax (Roth), under SECURE 2.0. There is not enough information to know whether traditional or Roth is more desirable for OP’s kid, but what is known is he chose Roth for other retirement investments.

His income, we hope, is lower now than it will be in the future, which is why I suggested he fund a Roth three years ago. I don’t know anything about a SEP IRA, but that sounds like a good option for him.

He has an emergency savings fund, although I don’t know how large it is, and I hope that he moved it out of BOA into a 5+% brokerage at Vanguard, where his Roth is. He talked about doing that. I’ll ask that before I give him this new infusion of money, though I really don’t want to condition the money on him doing what I tell him.

As I said before, he’s good with money, but he doesn’t know all the ins and outs. For instance, when rates were 2.6% he said that he’d pay cash for a house, and I had to tell him why that wouldn’t make sense (though I get his no-debt way of thinking). I just want to grow his knowledge of money. I’m still growing mine!

The main difference between the SEP IRA and the Solo 401(K) is that the SEP limits contributions to 25% of income but the maximum contribution is much higher. So the choice of which to use should consider which works better with their particular situation. The SEP is definitely better if you have a high income (>$100K), but not necessarily at lower income levels.

This is when you do want to max your retirement accounts (if feasible) because once your married and have kids and paying a mortgage and baseball and soccer and hockey fees, you may have to cut back on the 401k to just the match amount just to live for a while. Input picks back up later in your middle years as your earnings increase and your kids gradate and get off your dime - then you can really start maxing it out, especially after 50. But those early years make up for the loss in the middle years - look at any compounding interest chart and see if you invest for 10 years early, it will make more money than 20 or 30 years later.

At the same interest rates, a monthly investment over ten years and then held with no additional capital added for thirty more years will significantly outperform that same monthly investment made over thirty years. The additional ten years is HUGE!

Both of our kids started early with some money we gave them. Not a huge amount but it grows and grows. Now they put money on on their own. Compounding interest is such a great thing. Lol.

Our oldest is still in college but we decided the first few (3?) years of summer jobs we would fund their Roth IRA. It gives us a point of good conversation as he watches what it does and learns about investing.

I think starting early is key. The above reasons by @threeofthree are good ones. And from our personal experience in 2008, we were glad we could drop our contribution amount to save more cash because it seemed every three months more people were let go at work. This was after everyone got a pay cut as well. And then there was another pay cut to all during COVID. We were happy we both started saving for retirement in our early 20s.

It depends on the specific rate of return. For example, with a near 0% rate of return, obviously 30 years of deposits has a ~3x higher net than 10 years of deposits. However, with higher rate of returns, compounding interest gains dominate over the investment dollars, so 10 years of earlier deposits becomes more valuable than 30 years of later deposits. The break even point for first 10 years to be more valuable than next 30 years seems to be a little over a 6% rate of return. Specific numbers are below.

10% annual rate of return (historical average for total US index)

1 . Deposit $10k every year for 40 years – $4.6 million after 40 years

2. Deposit $10k in years 1-10, Deposit $0 in years 11-40 – $2.9 million after 40 years

3. Deposit $0 in years 1-10, Deposit $10k in years 11-40 – $1.7 million after 40 years

7% annual rate of return (historical average for market after inflation adjustment)

1 . Deposit $10k every year for 40 years – $2.1 million after 40 years

2. Deposit $10k in years 1-10, Deposit $0 in years 11-40 – $1.1 million after 40 years

3. Deposit $0 in years 1-10, Deposit $10k in years 11-40 – $1.0 million after 40 years

5% annual rate of return (current fixed income rate - expenses)

1 . Deposit $10k every year for 40 years – $1.2 million after 40 years

2. Deposit $10k in years 1-10, Deposit $0 in years 11-40 – $560k after 40 years

3. Deposit $0 in years 1-10, Deposit $10k in years 11-40 – $680k after 40 years

1% annual rate of return (fixed income after inflation/tax adjustment)

1 . Deposit $10k every year for 40 years – $490k after 40 years

2. Deposit $10k in years 1-10, Deposit $0 in years 11-40 – $140k after 40 years

3. Deposit $0 in years 1-10, Deposit $10k in years 11-40 – $350k after 40 years

High interest savings account may beat CDs - Wealthfront is currently paying 5.5 percent if you sign up with a referral. Does he have 6-12 months expenses in an emergency fund? That would be my priority if not - and into a high interest savings account. Then max out retirement funds (you say he is doing this).

If he has both an emergency fund and a retirement account maxed out, then save for future goals like house/engagement ring/wedding etc. Wealthfront lets you subdivide your cash account into categories (emergency fund, house downpayment, travel, etc) which is helpful seeing where you are in your goals. Depending on timeline I would do the high yield savings and stocks, watching stocks closely for a down turn. I just reallocated our kids 529s because they were way too conservatively invested (one graduated, one graduates next year, and one is a sophomore) and they have really jumped up in value. Like anything, watch closely.

For sure. I should have said at historical market rates, as low rates are impacted in the way you allude to. Six percent isn’t really the break even point though because you need to put three times the amount of your own money in to get the same final number.

Another way to think of this is what interest rate you’d have to get to break even on the same dollar amount invested.

If you started with $1000, added $1000 every month for ten years, followed by nothing for thirty years, and were able to earn historic inflation adjusted market returns, 7%, you’d have roughly $1.275M.

In order to end up with the same amount, while only investing the same amount ($333/mo x 30 years), you’d have to get returns over 13%.

Give him a copy of J. L. Collins’ “The Simple Path to Wealth” - it is comprehensive, readable, and able to be absorbed over a weekend.

Then he’ll have the tools to know what is best for his situation.

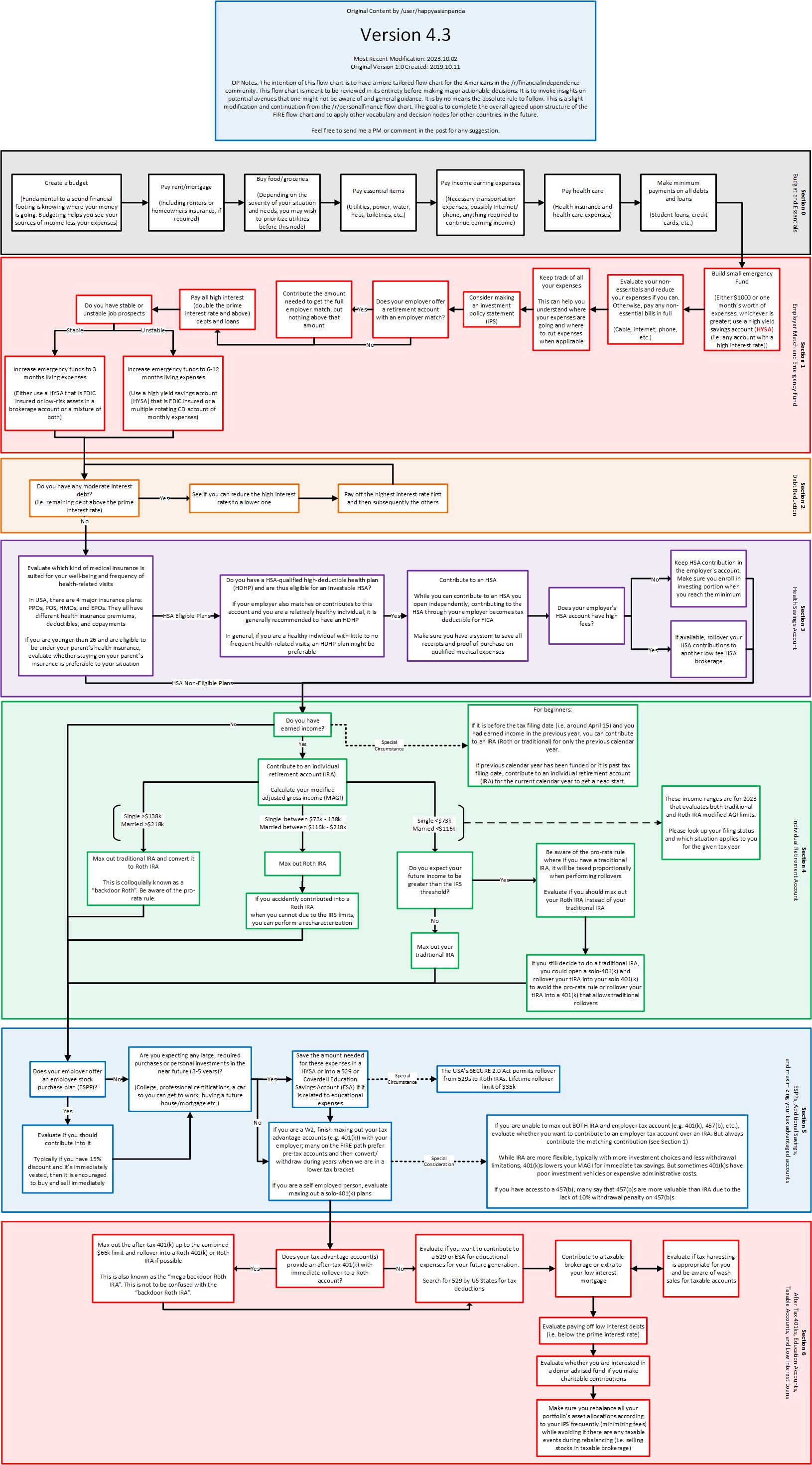

(There’s also a simple financial flow chart that is easy to reference, but it’s essential to have an understanding of why a particular choice is beneficial, and what one’s personal situation warrants rather than blindly following any path. Which is why I would highly recommend gifting the book as he’s starting out.)

Vanguard index funds. I’m in their S&P 500 index funds as well as an extended market index (that’s more volatile; wouldn’t put $ there for near-term use). We moved most of our cash from USAA (STILL under 1%) to Vanguard brokerage. It sits there making a lovely 5+%. I did the same thing with my smallish personal account.

{kind=link}