I am always glad that we bought our 2024 Nissa Ariya EV now, while I am young enough to learn all the bells and whistles. I love the Birds Eye view when parking, the heads-up display on the windshield , automatic headlights and windshield wipers, the driver seat moving back to help you get out of the car, the side mirrors folding in when you leave the vehicle(which lets you know that you didn’t forget to turn off the engine! ask me how I know… ![]() ) but I have had a little trouble getting the cruise control going correctly. The system alerts me when the speed limit changes and I can push a button to adjust the control to that new speed..but I am still figuring that all out. There are almost too many options!

) but I have had a little trouble getting the cruise control going correctly. The system alerts me when the speed limit changes and I can push a button to adjust the control to that new speed..but I am still figuring that all out. There are almost too many options!

2 Likes

Reading this thread, it seems that it could be a good idea to time that new car acquisition for a time when you’ll drive a lot – so you can “train” yourself on all the bells and whistles, using them enough that you remember how they all work.

It’s so irritating to know a feature exists – because you’ve used it – and not be able to find/set it again!.

3 Likes

With all of the features, sometimes the control is buried in a bunch of touch screen menus, and sometimes it is a button hidden in plain sight in a sea of other buttons.

4 Likes

lol. I relate to this quite a bit.

Twice this week I’ve discovered new functions on my vehicle that I bought in June.

I plan to have this car for many years, but clearly I need to examine every niche of this car in my garage one afternoon.

1 Like

My H is figuring out the controls on his new car, which are different from the ones on the loaner he used while they were applying a coating on his car. I’m sure he’ll figure out the ones he cares about (having the seat go back when he’s ready to exit the vehicle & having mirrors go in so they don’t get hit by folks passing by or parking nearby). He’s enjoying learning so far. I have not tried driving his new car as it’s still HIS and I’m happy to let him explore.

2 Likes

Today we had our 10K maintenance visit (“free” with purchase, though we did a 5k oil change on our own). The loaner ended up being almost the same car, including exterior color. However it was missing some features we have, convincing us that (for us) they were worthwhile splurges.

-

Digit rearview mirror - even my tall husband missed it, grumbled about the rear headrests blocking the view. (Workaround is possible - we have friends who had similar issue on a different car and simply removed the rear headrests. Like us, they rarely have rear passengers.)

-

Light colored interior - neither of us likes all black leather (or immitation leather) seats… and today’s hot weather reminded us of that.

The car did have a lot of other bells and whistles we like. Admittedly we are now spoiled. We do hope to keep this car a long time, so I’m glad we both like it.

1 Like

Audi of America, which imports each vehicle it sells in the U.S., is implementing some hefty price increases across its portfolio for the 2026 model year as the German luxury brand grapples with tariffs.

The price increases for 2026 range from $800 to $4,700, depending on model and trim, and come amid a U.S. sales slump at the Germany luxury brand.

3 Likes

Car prices hit nearly $50,000 for first time as vehicle costs surge | Fox Business

Americans Are Falling Behind On Car Payments Like It’s 1992 All Over Again | Carscoops

1 Like

My car is paid off next summer (I took a many years loan to ensure I could handle the payments so it’s been a looong time coming). I have just over 70k miles on it (thank you Covid or it’d probably be at least 100k thanks to move to virtual meetings at work). I assume I’ll keep it for at least another 70k, maybe another 100k miles which will probably take even longer as I drive less each year. That means I’ll own this car more than 15 years. I assume many others will do the same at these prices. Wages have not even close to kept pace for most people. But tell me again how Elon musk is worth a trillion dollars. At 100,000k per year it would take 10,000 years to earn a billion dollars - a trillion is too many zeros for me to even contemplate.

3 Likes

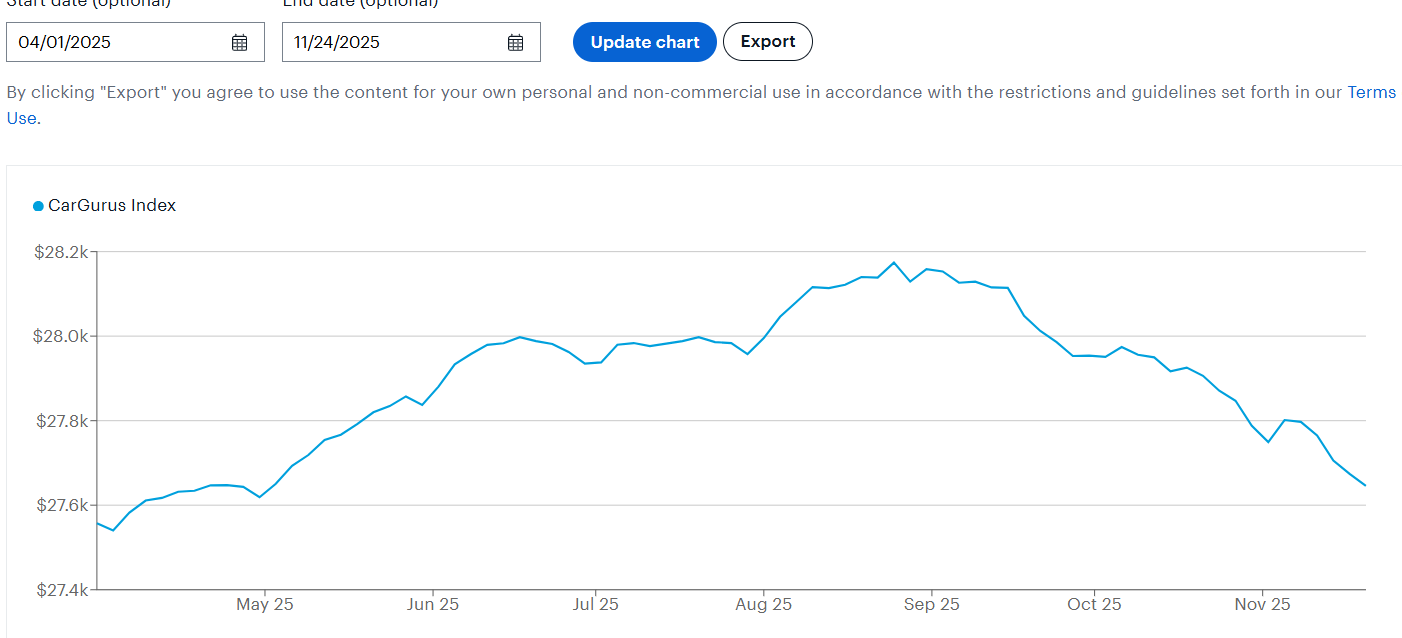

The CPI inflation report paints a different picture, with a less than 1% year over year change in aggregate price of new vehicles, and a small decrease in aggregate new vehicle prices since this thread started in April. CarGuru used car prices also show relative little change. Their aggregate index is pictured below.

I suspect the difference is the CPI calculation compares specific car models – how did the price of car model x change over the past year? While the $50k KBB figure is average transaction price, without considering car model. Said differently, people are more likely to buy higher end car models than last year, rather than prices of same car model increasing. This is consistent with other metrics of the economy suggesting overall spending is being more driven by wealthy persons than in previous years.

1 Like

I read auto news daily and it’s stayed flat just below $50k but my company sends us articles each day so I included. Today it shows $49,911. Down .5% from April 1. But the article shows otherwise. Which source is correct ? OEMs have tried to hold but some can’t due to tariffs.

I know loan defaults are up and I know many OEM captives are turning down marginal buyers. Many are losing many millions a month from loans made during the COVID era.

Auto News Daily uses a different computation method from KBB, so prices do not match exactly. It’s my understanding AND uses an aggregate of list prices - discounts across all car models, KBB uses an aggregate of average transaction sale price across all car models, and CPI uses how transaction sale price has changed from previous year when controlling for the same car models. AND new car price history is pictured below:

It has also been the case that, over the past several years, many companies have discontinued lower cost models without replacement.

2 Likes

Yes, that was what I was alluding to. Planet Money had a podcast on consumer spending and K-shaped economy a few days ago. Some quotes are below:

MALONE: Uh, fair point. Anyway, OK, look. A few things in addition to this, like, insulation factor have also been going really well for people at the top. So, like, this year, their wage growth has been strong. For low-income households, though, growth has been slow.

PATKI: That’s an important resource that supports spending-- paychecks. So that is another factor. And finally, you have changes in wealth. Homes, stocks-- these kinds of assets have become more valuable in the last five years, and they’re likely to be much more important in supporting consumer spending for households at the top of the income distribution.

GONZALEZ: Yeah, people who own homes, their homes have been appreciating in value in, like, wild ways in recent years. And then people who have stocks-- the stock market is doing really, really well. And that gives wealthier people the confidence to spend even more generously.

…

ATWATER: Oh, so the epidemic had barely hit, and economists were predicting how the recovery would take place. And so you had those saying, oh, it’s going to be a V-shaped recovery. Everybody’s going to do well. Others said, no, no, no, we’re going to have this long, pronounced decline, and then it’s going to move up, so it’ll be like the letter U. Others thought it was hopeless, and it was just going to be an L. And I was like, no, it’s going to be K.

…

ATWATER: You know, we-- today, we have twice as many car models that cost over $100,000 than cost less than $30,000. Those driving used cars on the highway see that every day. And so the overabundance at the top is incredibly visible and demoralizing.

GONZALEZ: Peter says we have a bifurcated economy. Basically, there are two different economic experiences existing simultaneously.

MALONE: And companies are focusing on investing in their higher income consumers, like giving them incredible credit card perks, while low-income consumers are defaulting on their credit card debt. The average price of a car right now is $50,000, while car loan defaults and repossessions are on the rise.

1 Like