Perhaps. As noted upthread, the only way to get an ironclad value is to put the property on the market and solicit offers. But if you want to use quick sale value, according to the IRS definition that you provided earlier, the starting point is fair market value. So you’re going to have to come up with your best guess of fair market value anyway.

I think that anyone who pushes quick sale value as a proper way to assess real estate for financial aid purposes, in order to be credible, needs to provide a compelling rationale for doing it that way. So far, I haven’t seen that. And no, I don’t think that those values are being challenged, for the same reason that most values that are straight out fraudulent probably aren’t being challenged: it’s awful hard to screen every one of these forms and put the time and effort in to determine which real estate values are legitimate and which are not. Heck, on the FAFSA, investment real estate isn’t even broken out as a separate category; it’s lumped in with all sorts of other investments like non-retirement investment accounts and 529 college savings plans. In most cases, the only thing standing in the way of not doing it the right way is your conscience.

@roman…".Really, there is almost zero room for interpretation on these forms". I totally disagree, want to discuss FMV of PE carried interest or forgettable option loans tied to an underlying security ? Good, neither do I, but the point is there is huge room for interpretation in some instances.

@bk…sort of disagree. Why wouldn’t quick sale value be used if by proxy (not literally) the school is saying use that asset to pay ? Ie: liquidate it.

@jell…I hear where you are coming from, but as has been said, high income will take you out of the aid ballpark before assets even come into play.

Also for those looking for actual statements from FA officers . I’m not trying to make any point here, just pass along a quote.

" the fafsa and profile are not the times to be bragging about the value of your RE holdings "–very selective LAC central NYS

Even if that were the case, the liquidation wouldn’t have to be a sell-at-all-costs, fire sale transaction, which is what a quick sale implies. If the school really wanted you to sell the asset to get cash (as opposed to using equity to get a loan), it would be in everyone’s interest (including the school’s) to do an orderly sale that yields the highest price.

Makes perfect sense to me, because “bragging” suggests inflating the price above a realistic fair market value in order to impress others. I wouldn’t do that, and I also wouldn’t report a value that I knew to be unrealistically low.

@thumper… I’m off topic here , but question re: Your quote:

“Your kiddo will get that ED acceptance and financial aid package…and will have a very short window of time to decide whether to accept it. The trouble is…this ED financial aid will be the only package you will have. It might be the best one he could get…and it might be the worst. You will not know when you make that decision.”

I’ve always thought the same, but what if an ED app and a few EA apps all go in on Nov 1, wouldn’t all the FA packages be back by yr end ? Giving some basis for comparison?

But we know the school is not going to be involved or interested in an orderly sale. Therefore the asset has to be discounted to the current FMV, which is liquidation value TODAY (remember we are playing by profile/fin aid rules…snap shot in time) which would be a quick sale value.

When we speak of aid comparisons, it usually includes RD offers, which come months later.

Quick sale is generally under duress of some sort. Colleges are not asking you to fire-sale your home to pay debts or get out of town for a new job. They simply want to know what a fair value is. And then the calculations down to net. So, not whatever anyone will pay in a week or two. Rather, what an ordinary selling period in that area would bring, for that property, in that specific property’s present condition. And not some calculation of how economic factors affected the sum total of homes in your state. This particular property.

You can look at how various sites discuss Quick Sale Value.

@erins dad. By “in” you mean accepted EA, yes, otherwise it is moot. Anyway, I’m going to re-phrase my question in a new thread. sorry for the highjack.

You guys make some great points. I think I might have valued my home more than I should have. I should have spent more time looking into it. Oh well. Kid will have to deal with heartbreak. His top top pick wanted a CSS profile. Looks like that will not be an affordable option. A value hair cut just might have made the difference.

The IRS uses a 90 day framework. The overwhelming majority of assets that get listed in the “offer-in-compromise” system aren’t liquidated, there just needs to be an assessment of their worth, as in this case.

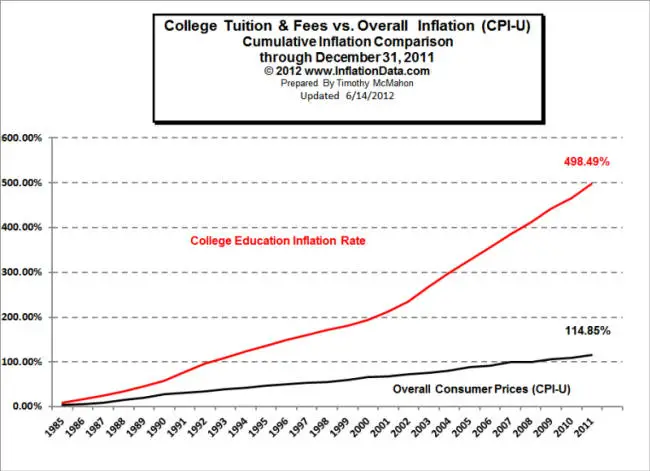

Well, this probably should be another thread, but I think you’re looking at it upside down, the way the schools want you to. Try this thought experiment: They’re not giving aid, they’re agreeing not to rip you off for all you’re worth and to move the number towards what college should cost today in a sane world. Look at the chart below, they’ve raised the price of education far faster than anything else in the economy, including healthcare. This way the default is extortionate costs, and you have to beg for relief. Imagine if the cost of health insurance started out at 60% of your take home pay and you had to beg for a reduction. I’ll play their game because I have no choice, but I’m under no illusions about who’s getting played. As has been said many times, they’re the professionals at this.

I don’t remember if somewhere in this thread you mentioned what kind of schools your child is applying too but most elite colleges that guarantee to meet need will come up with their own value for your real estate through any number of methods. If you challenge it some will acquiesce because they don’t want the fight but many won’t. Real estate is a major trigger point for many financial aid directors. Taking 20% off for “quick sale value” is not a valid reason to change a property value in any of the many offices I have worked in. In fact, if a family tells me the they did that it is going to make me skeptical of the rest of their application and I would be going through their LLC with a fine tooth comb to make sure we did not miss any “add backs” or other entities or assets.

Just be honest! Put the FHFA value and explain that is what you did. You will get a lot further with honesty than trying to “play the game”. If you want to appeal because they are illiquid, or would have large capital gain taxes, or your income would not support borrowing go ahead and I would strongly encourage it but I can assure you that any school that requests your LLC return will do their own due diligence on price and if you way undervalued your assets will have dug yourself a big hole that will impact the rest of your dealings with the office.

At elite schools we actively work to make it as affordable as possible for your family but only if we feel the family if being upfront.

P.S. Do not EVER listen to a “FA consultant” and most CPAs and Financial Advisers are equally as clueless in financial aid policies.

P.P.S. Most of the increase in college cost has been in the public sector because of state cuts. Private costs have outpaced inflation but not nearly as much as at state schools.

@jellicus, I realize your data has some value at a glace, but is it fair to compare college tuitions to consumer goods upon which pricing has so many other variables and pressures (such as country of manufacture, advances in automation, international monetary effects, etc)?

@bk … if you don’t think a discounting mechanism is applied to all FMV’s is some way or another you are mistaken. n.

I would have no problem defending a discounted value, if indeed there is one, any appropriate asset to a FA officer or anyone else.

In fact, if the reverse was the situation, and you were trying to borrow or margin a diversified real estate LLC the loan to asset value would be discounted for the very same reason !!

The Fafsa/css is flawed in may ways. But if these are the rules an applicant must abide by, at least do so intelligently so as to not disadvantage yourself or your family

@bschooltotech, Thanks for an informed and reasonable opinion. Can you elaborate on how capital gains tax fits into this picture? And does the active rather than passive nature of the LLC or the commercial designation of a property have any effect on how it’s treated?

In my readings of articles on the cost inflation the state cut theory is debunked. One article cited a study that in the UC system there was a 10% increase in instructors over 30 years and a 500% increase in administrators. Look at this chart from 2012, in just 4 years the Ivies and their peers, including my son’s EA, have gone up over 25% and are over $60k. This is unconscionable.

These are one-size-fits-all forms. Of course they aren’t going to be tailored to some (or maybe even most) financial aid applicants. This discussion started with a post about using “quick sale value” as a method to value investment real estate on the Profile. Along with others, I have tried to explain how this is not an appropriate “discounting mechanism” to use for financial aid purposes. Current fair market value shouldn’t be a difficult concept to grasp. There’s no reason to make this more complicated than it might already be.

@bstech…"can assure you that any school that requests your LLC return will do their own due diligence "

Do you actually work in A FA office ? if so, it would be interesting to see a hypo of one of your offices RE LLC valuations…( bet it has a PV discounting mechanism of some type on it.!)

{kind=link}

{kind=link}

{kind=link}

{kind=link}