From the bogleheads.org articles I skimmed, it sounded like some charge a 7-12% up front commission or fee PLUS an annual fee of 1.5 to 3% plus other expenses.

@bluebayou makes a great summary statement essentially saying it’s about risk and debt tolerance and how one feels towards both. As a financial advisor for the past 30 yrs, I’ve seen so many people on opposite sides of the argument.

It also depends on how long you plan on staying in a home. If you’re there for less than 10 yrs, unless you put a ton down, you’re essentially renting anyway or trading equity with the bank (albeit you’ll likely get more lifestyle for your money).

Range of options is so extreme. Have clients who buy with cash (from stock options, down sizing, significant growth in investment accounts) and one guy who said his goal was to pass with the largest mortgage possible (yes he likes leverage) and have it paid for with a life insurance check. He invests what he would have paid towards mortgage balance and could write a check to pay his mortgage off but chooses to keep the compounding and growth going. Always refis for lowest rate possible (seems like a lot of hassle to me but that’s his thing).

Very much based on one’s attitude towards investing and debt.

I sometimes think, for a moment, that a mortgage is a good inflation hedge. The moment passes, and I really really like not having a mortgage.

Our credit score has taken a hit because we haven’t had any installment credit for almost 20 years  and because I closed an unused card. It has not fallen enough to make our insurance rates higher, so I don’t really care.

and because I closed an unused card. It has not fallen enough to make our insurance rates higher, so I don’t really care.

^ It’s a crazy system when your credit score goes down because you have closed unused cards (we did that too). You should represent less risk, therefore a better score because you can’t access the balance on those closed cards. But it doesn’t work that way. The credit folks want you borrowing.

As long as your credit score doesn’t effect rates on insurance, mortgages, car loans, etc., it’s mo big deal.

Hi all,

So, I skimmed through a few pages, and most said that we need to have the same retirement income as when we are working.

I have always felt that we need a lot more when we retire than when we were working. The entertainment budget (eating out, vacations, movies, concerts, entertaining with friends) would go up significantly since we have more time. And also, what’s the point of retirement? I want to be able to do and enjoy life more than I were working. No?

We have on average 25K budgeted for vacation each year with 2 kids now (1 is now freshman in college). This gives us a couple of decent trips per year, plus maybe 4 mini trips for kids’s club soccer. Every 3 years we go to Asia and that particular trip is about 20K, lots of gifts for the relatives, and of course we pay for everything and everyone.

If we retired, I imagine the travel budge would double. I also heard that if you want your adult children to travel with you, you have to pay for them AND their family. Anyone cared to share their experience here?. Plus the chances for the kids to live by us is small, so need to add to the travel budget just to see the kids and their offspring (if we are lucky).

We are 48 years old, we work at the same company for over 20 years - my company has very decent pension. I just looked up and it say that if I work for another 10 years my pension would be 11k/year for the next 10 years, then it goes down to about 9K/year as i hit 80. Hubby’s pension isn’t that great but his company still has it, he thinks it will get frozen soon.

Anyways, I think we would need about 5-8 millions to retire comfortably and maintain the lifestyle that I imagine for us. We are not there yet but hopefully in 10 years we will.

@Nhatrang Wow. Your travel plans in retirement are drastically different than ours! I like yours better but could do without paying for extended family members. I draw the line way before that! A pension of $11K/yr doesn’t sound that great, but you and your husband are lucky to have it.

@bigmacbeth - my mistake, it’s 11K/month, basically half of your current salary by the time you retire (not including stock option and bonus).

What about State income taxes? Aren’t those part of SALT, too?

I realize that credit score marketing is all the rage, but what am I missing? I have never, ever looked up my credit score. And now just retired, why would I care what it is?

@Nhatrang Welcome! What a generous pension you have. Without knowing your cost of living, sounds like your savings goal would support a nice, post-retirement lifestyle.

We do treat our young adult children to occasional trips with us - having them along enhances our experience and they can’t afford it at this stage of their life.

It can affect how much you pay for insurance, or if you can even get insurance (depending on where you live, I think some states don’t allow it).

If you carry a balance on a credit card or want to get a new card, it will affect the interest rate or if you can get the card at all. If you want one of those super-high reward cards, or a card with a big enrollment bonus, you need a good credit score.

And maybe you will never have to get a job or rent an apartment after you retire, but your credit rating will affect that as well. Want to rent someplace fun for a couple months? Better have a good score.

My credit union emails me my credit score every month. It moves up or down 10 or 15 points for no discernible reason, but hovers around the same number.

Most responsible adults have credit scores in the 700s or higher IME, so you probably don’t have anything to worry about. I like to know mine though.

@notrichenough and @IxnayBob – How do you find out how credit score affects insurance costs? Are we talking about homeowner’s and umbrella, or auto, or both?

I don’t have any installment credit either, but the FICO score as reported by my CC company is high.

My CC company reports a score out of 900, but I thought credit scores were expressed on a lower scale. Should I doubt the score reported by my CC issuer? The fine print says the info is provided by Equifax, so perhaps that alone is reason to be suspicious.

There are a number of different models used to compute credit scores and they have different ranges. When your credit company reports yours they should be telling you which model they use and the range of possible values.

“FICO” is short for “Fair Isaac COrporation” and is trademarked to them, and has a range of 300-850 (who knows why? Apparently they never heard of normalization), and is the model most people have heard of because they were the first (and for a long time, only) credit score model, so it has become something of a generic term for credit scores, like xerox or kleenex. Now there’s lots of models for different uses by different companies, so you have to be careful when looking at the number.

Last we looked, we have credit scores in the 800+, tho we paid off mortgage over 7 years ago and it was only debt we ever had.

We have a Home Equity Line of Credit for $250k, which we’ve never ever used but could if needed. Never paid a dime to get or keep the HELOC.

In retirement, we go on about 4+ trips/year, which suits us well. We offer to have our “kids” join us and sometimes they do. We are paying 100% of D’s expenses as health issues have prevented her from ever holding a full-time job. We have “enough” for us, even with supporting D.

H has a pension considerably less than $11K/month and is very grateful for it. I have no pension and will get modest SS at age 70 (to the extent it still exists and isn’t restricted by folks earning “too much”). He’s pension is enough for us to dine out often, travel, pay taxes and all our expenses.

Here’s a good article:

https://www.uphelp.org/pubs/credit-scoring-insurance-unfair-practice

Apparently only CA, MA, and HI ban using credit scores for auto insurance, and only MD and HI ban it for homeowners. (According to this article, it could be out of date).

If your state doesn’t ban it, I’d say the chances of your insurance company using your credit score is close to 100%, although they probably go to some effort to hide that fact.

ETA: Ha, I was close:

https://www.naic.org/documents/consumer_alert_credit_based_insurance_scores.htm

If you have good credit, closing out a card or two isn’t going to bring one down to a point where you need to worry about getting dinged on insurance rates, credit card rates, short term rentals, etc.

Some of our CCs have ridiculously high limits. I’ve heard you can get your high limit transferred to a card you’re going to keep before closing one you don’t want/use (if issued by same institution).

We honestly have more cards than we want or use.

Sometimes the CC companies close our unused ones, sometimes we do.

I’m ambivalent about the high limits. Mostly we don’t use them but the have been helpful when we wanted to charge a lot in the past. Most of the time, we only use a very small fraction of the credit our cards offer & always pay if off in full every month.

I think some of the credit card companies give high limit is that they have a pretty hefty interest rate, and would love for someone with a good credit rating to pay some of that when they don’t pay it off in full the next month.

Credit Card companies also make money via transaction fees from merchants, averaging 1.75%. So, the higher the credit limit they give you, the more they hope you spend regardless of whether you pay off your monthly balance or not.

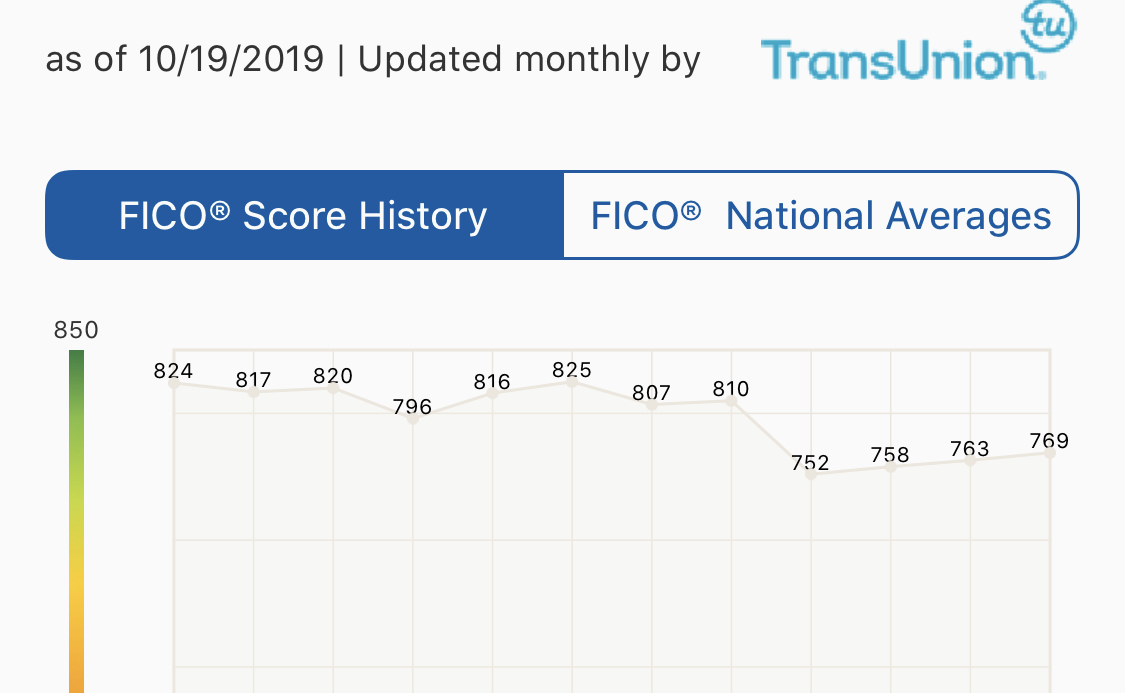

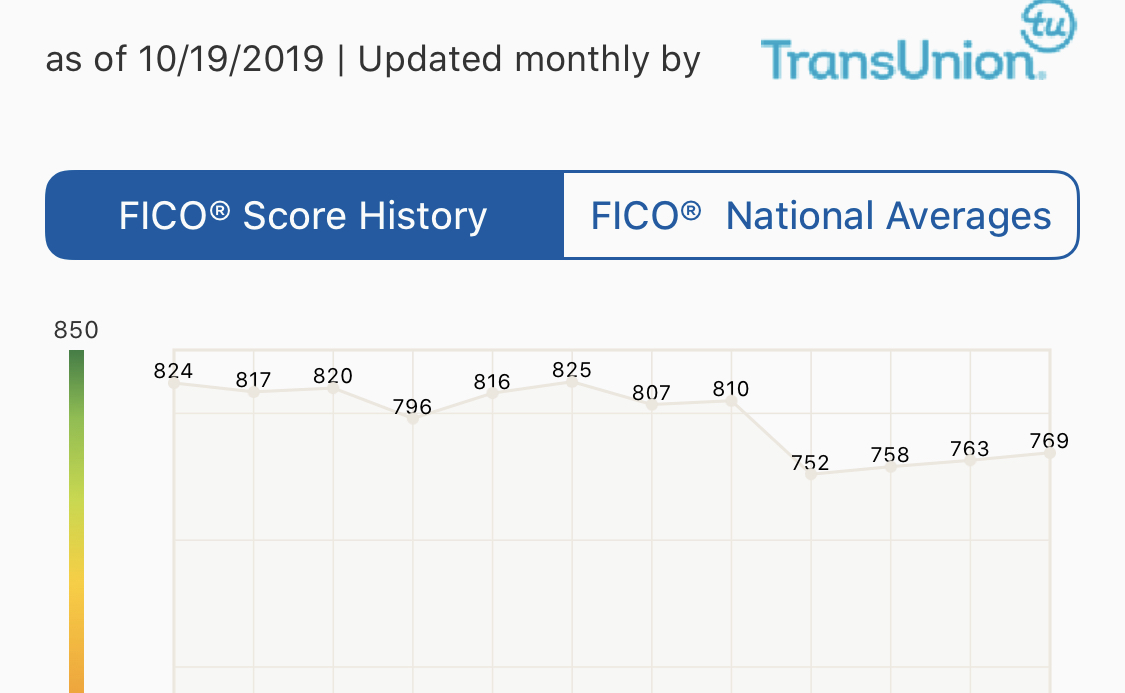

3 C0 D60 F1 6925 4 D3 F 98 B3 4 B886582851 C — Postimages

You can see our score bouncing around for a while, and then a dramatic drop as I closed one of the cards. It’s working its way back.{kind=link}

{kind=link}

We are not getting a mortgage, ever, and our credit score is still pretty good. That said, the fact that it’s not perfect is a joke. We have not had any debt for years, paid for multiple tuitions out of cash flow, paid cash for our new house even before selling our old house, etc.