I completely understand what happens when you end up penniless in old age. My now 93 year old father blew through the over $1 million he got selling his house in just a few years. He spent it on his care. The assisted living bill was high, but he also contracted personal aides for several shifts a day and that bill was what made him broke. I was not involved in his finances at the time as he was of sound mind and made this decision for himself. Note, these were not medical aides, but rather “comfort” aides, that he wanted. He is now in a nursing home where the government is paying for his care. He is getting good care and his all his needs are met. I am still not involved in his finances, so I don’t know the details, I assume his SS payments are used up first and then Medicaid pays the rest.

I consider his story a lesson in two ways. One to spend wisely on your own care. Secondly, the world won’t end if you end up broke.

Having worked in skilled care/rehab, a small portion of his social security money is available to him for personal expenses/incidentals - but from what I understand it is not very much.

Hope your dad is comfortable in his care situation. DH’s grandfather and father both were in skilled care (nursing home) with the government paying for their care. GF died at 96 and F died at 92. They got very good care.

I am not involved in the day to day - he has an elder care lawyer who is. There is money to pay the lawyer and anything critical (new phone when his phone broke, etc.) His funeral expenses are all pre-paid. I am happy with the level of care he receives. He reached a point a few years back where he just decided to be unhappy about everything and anything, and that will never change.

Sometimes in this thread I would like to hear from those (I know you’re here and I see and feel your situation) who weren’t so fortunate to have high paying jobs or the ability to save $ to land at a million + to live on. Or the financial savvy to think decades ahead.

I don’t begrudge anyone who has more but the fact is there are A-LOT of Americans who fall in this category.

Would be interesting to hear from the mid-crowd. It’s my opinion that banking 3 million is not the norm.

My concern is basically - not having lost all I’ve gained in life - it could help my kids and their kids and kids for many years perhaps - like when you see something that’s been passed for generations.

But I also know, often times things costs more than you want and in certain healthcare scenarios, you need a lot of money to get the care and housing you need and the government doesn’t help - or at least until you’ve gone broke and then they help, but not to the level you necessarily desire.

To work hard and to have it just be gone - for me - that’s not good. For others, and it’s their choice, it’s fine.

Even the “giving pledge” billionaires don’t want to lose principal - they simply want it donated to make the future world better. I can’t do that myself with my little bit - if I’m broke.

Yes, there are tables and most likely need to spend their principal - but not having to is far better than having to - is the point.

My plan is for my money to outlive me. Those tables are for people trying to figure out how they can time their money to last an average lifetime - which they may or may not exceed.

And yes, I’d like to help generations to come and if I can save enough, I’d eve like to endow a scholarship (small, but something). My cousin has at Northeastern and that’s a beautiful gesture.

That’s me. We have more than $1M if you count our house, but I don’t count our house as part of retirement.

When we were both working our household never made six figures. But I always have been a saver, and compounding is a great thing. We didn’t have a “number.” Also, we both have pensions so that helps.

Pension certainly does make a diffence when planning for retirement. Ours is lots less than original early career projections, but we’ve had a lot of time to adjust to that.

My family story of “not millions”. My grandparents had decent savings for their generation. As their health deteriorated, my divorced mom quit her job and retired early… moved them to her apartment. She did an admirable job caring for them a few years before having to start nursing home care, first for grandmother and then a few years later after my grandmother died my grandfather went to nursing home… Mom’s actions did reduce er parents time in nursing homes. But the last year or so my grandfather was on medicaid. So none of those savings went to my mother, except I think a year or two they gifted $5k. Mom spent most of her last two decades in Section 8 low income housing. Always humble and gracious, never a complaint.

Bottom line for me is that I am not hung up as much about taxes (especially for my heirs) as some people. I’m just appreciative that my mother was able to stay independent and self-sufficient, never needing financial help from children .

I understand what RMDs are, and I have debated doing Roth conversions often, but never actually did. I do wish I’d contributed more to Roth when I was working.

I worry we might be in a higher tax bracket than I/we were when we put the money in. I also worry that my kids will be in a high tax bracket when they need to take the money out, if they are lucky. Additionally, if one of us dies, then the tax rate could be really high for a single filer.

I know - first world problems.

Another thing you can do, if your past 59.5, is to just take out more money now and pay taxes at your current tax rate. Lets say your in.the 22% bracket etc, you could take out additional funds up to the top of that bracket and then either invest that in a brokerage account or gift it to kids now. That would remove some uncertainty about later.

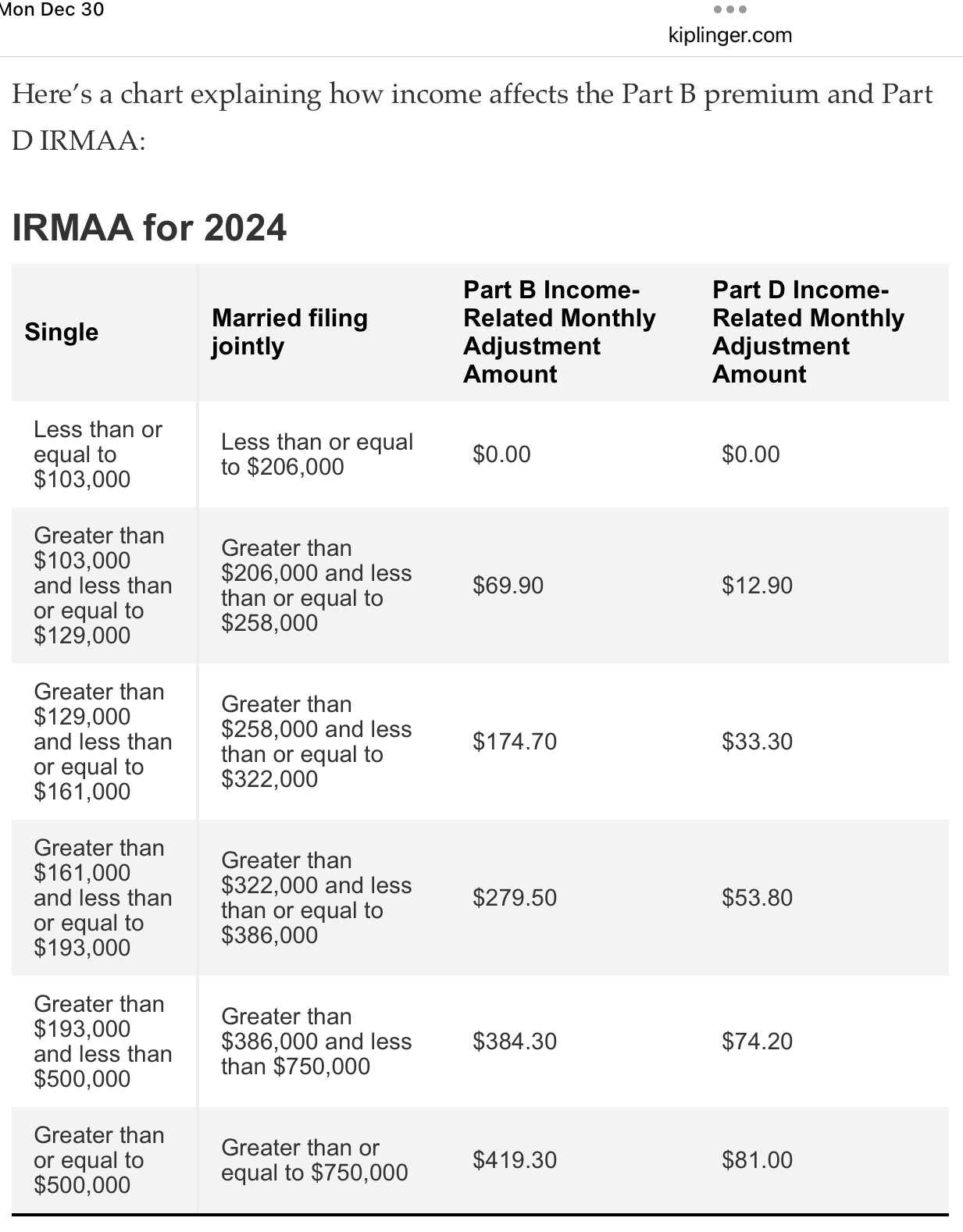

For the newer folks here, I’ll post an example IRMAA chart (exact values vary by year). IRMAA is the extra monthly “tax” you will pay beyond the base Medicare. Times two if both spouses on Medicare.

With very large IRA, it could possibly be a factor in RMD years. But for most retirees the risk comes from doing Roth rollover as a big chunk. There is a look back to prior filed taxes, so plan carefully if you are age 63+.

It’s still $185 base amount for part B each person pays. Then the above added as you said. I am always sticker shocked when I realize it is added on to the premium of part B.

Well, if I need 3 million for retirement I hope I don’t live very long!

I read @deb922’s post up above regarding her inlaws gift and I had a strong sense of deja-vu. When my children were in high school, getting ready to apply to college, my mother-in-law “gifted” her children with stocks. Great, right? No. We couldn’t touch it. She had gotten all of her children to agree to shelter the assets in their name in case she needed it to maintain her lifestyle. We were not in equal economic situations; we were the only ones looking at colleges and needing substantial financial aid; we were rich on paper but were living paycheck to paycheck. My MIL offered to help with college expenses for D if she got into Harvard, but only Harvard. She was waitlisted. Needless to say, I was not consulted about these arrangements.

My mother was very, very frugal. Mom established a scholarship where Dad worked and did a lot for various organizations in our community. H really doesn’t understand or want to continue that philanthropy. Mom had an excellent advisor (where I’ve left my account) and left an estate in excess of 2 million. I am very grateful for that. As far as I am concerned, it’s my money. H and I have a joint account with what remains of his mother’s assets (and note, there’s no stepped up basis as she gifted when she was living) but everything else is mine. If I want to give it to an arts organization or the SPCA, that’s my decision to make. We own two pieces of property, hopefully we’ll be down to one soon.

Life can be challenging. You never know what people are going through or why they are in the position they’re in. It’s not always about living beyond your means.

Ok, i understand no one wants to pay more but if your income is higher it makes sense that you would. And honestly, the overall yearly/monthly amount for Medicare premiums even with IRMAA added in isn’t that bad, especially compared to some quotes I’ve heard here from @MaineLonghorn, etc of $2000 monthly premiums with still high deductibles on their current insurance.

The worst cases are actually the lowest, standard bracket where with income from say 50-200k for a married couple, the yearly cost is $4440. Perhaps 8+ percent of total income. A couple fortunate enough to bring in 300k a year is only paying $8880 yearly or 2.9% of their income. And a truly rich couple binging in 700k is only paying $14184 or 2% of their income.

Yes, it costs more but these are hardly crazy amounts for someone with the means to afford them. Maybe its not actually that bad to make a little bit more and just go ahead a pay the differencein the end.

My current employee plan premiums are almost 8k per year. And others are potentially much higher with perhaps not high salaries.

The poster had mentioned Roth conversions but hadn’t done them. I was just giving other potential options to move some of that money around and minimize RMDs.

Absolutely, a Roth conversion probably makes the most sense. That’s what i probably will end up doing when the situation warrants it.

I am sitting here today toying with the idea of Roth conversions in the 22% & state @ 5%. (Nothing like the last minute.). I have so little headroom in the 22% that I am not convinced it is worth incurring the tax expense. Already filing as single, so I do not have the concern of MFJ posters.

Motivated by what will have to be higher future tax rates.

Once the ACA subsidy lapses, my annual premium will be $15K (2025 rates) for a HDHP with $6700 deductible. So interesting to see the highest Part B rates expressed at various income brackets.