Can someone explain in simple terms about the conversion? Is the idea that because it’s taxable upon conversion (but not later distribution) that you want to move money that has lost value? Doesn’t that lock in losses?

Agree about annuities being pushed by FA’s as they result in huge commissions, but disagree on Roth conversions being pushed by advisors. It’s in their own vested interest to keep more $$ under management, and a conversion is an immediate tax hit today, which means less for them to invest. (cash if fungible, so even if you pay the tax out of a bank account lying around, if that is your ‘emergency’ fund it should be replaced)

4 Likes

The idea is that one pays taxes on the lower value, in anticipation of the value increasing in the future.

5 Likes

If someone is currently in the 37% marginal tax bracket, Im not sure a Roth conversion makes sense.

You have to have a lot of retirement income to be in the highest marginal bracket in retirement.

Currently, the highest tax bracket for Married filing jointly is $751k. Using the 4% rule, someone would have to have a little less than $20 million to generate enough income to eclispes $751k.

Obviously tax rates can change and everyone’s situation is different.

2 Likes

By thise trying to get your assets. Not current advisors.

The - come have dinner on us - people.

So when you covert it over, it’s as a number of shares not a number of dollars?

1 Like

Yes, you convert in-kind.

A distinction without a difference. Both get huge commissions for selling annuities. Not saying that all annuities are bad, but one needs to be careful that teh seller gets comped. (Unless teh FA is fee-only in which case they might rec an annuity found online.)

Yes. I over simplified. Moving shares valued lower today means less tax to pay on conversion. (My apologies for the oversimplification. )

1 Like

No - the buy me a steak dinner people are selling Ruth conversions - as a way to get you to bring your assets to them.

I just noted the parallel to annuities - if everyone is pushing both - well buyer beware.

For some couples, the appeal of Roth conversions is to avoid excess taxation/IRMAA on very big IRAs at RMD age (more of a risk if down to one spouse, in single tax brackets).

3 Likes

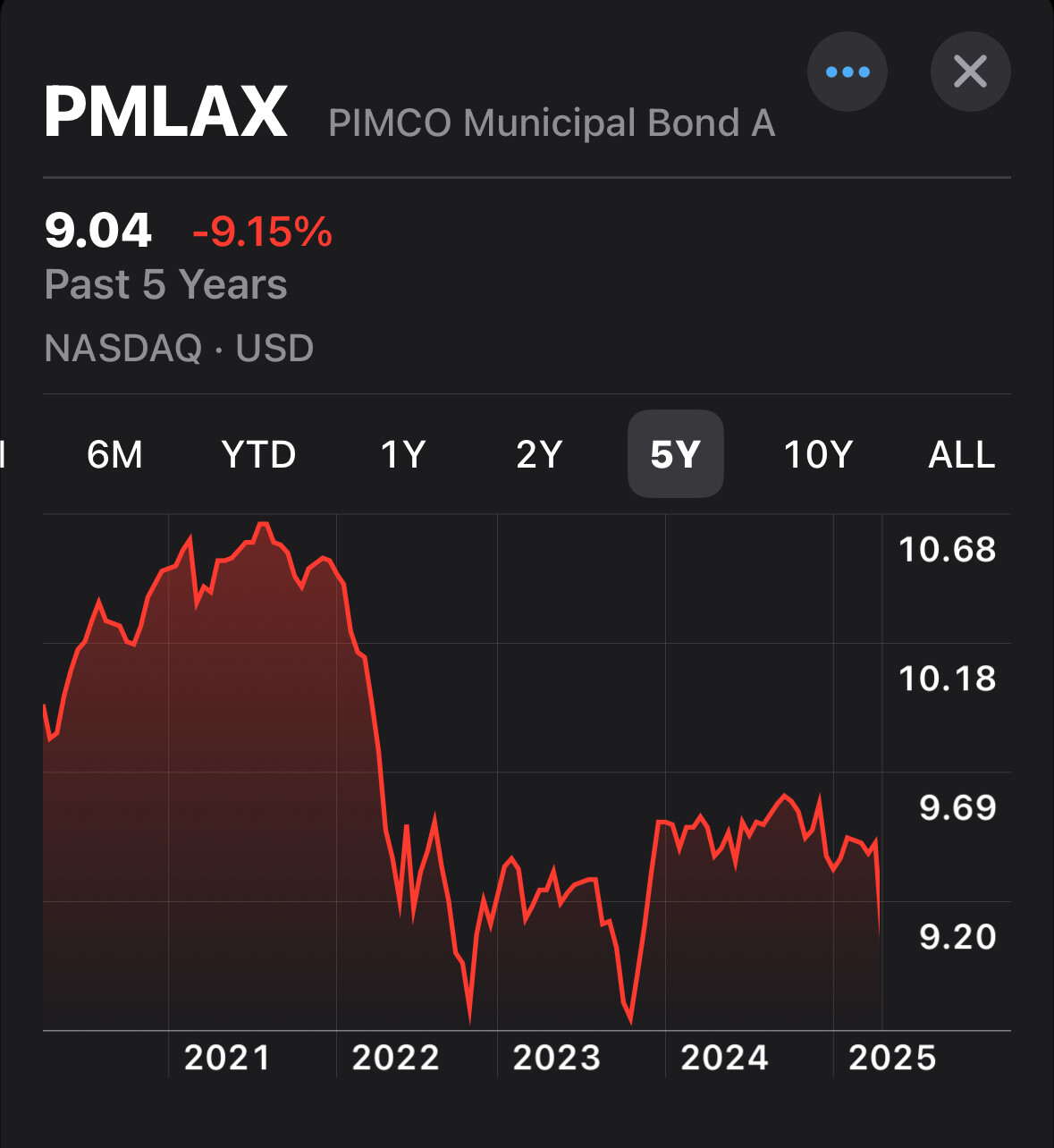

Municipal Bonds in the news…

https://www.morningstar.com/bonds/is-tax-exempt-status-municipal-bonds-risk

https://www.barrons.com/articles/muni-bonds-yield-8d33c0c5

From all three articles (factual vs political).

”President Trump recently floated the idea of taxing municipal bonds”

Tough Year for Munis…

Versus SP 500 same period in spite of recent downturn…

Tough 5 years for munis…

Versus SP 500 same period, speaks for itself…

1 Like

For those who own municipal bonds, you don’t worry about sell offs - except that you have a chance to obtain higher yields.

I own stocks - some have fallen - 100%. I’ve lost everything.

I’ve had bonds fall to 70 and rise to 110 and guess what - when they mature, they pay - you guessed it - 100. Pricing of bonds on the secondary markets adjusts so the yields hit what the market currently is. A 4% coupon may have been 96 a month ago and 93 today - that just means I get more bang for my buck on my next purchase (similar to a fallen stock).

This is why, with all the market turmoil and I am a victim of it with many of my stocks down 50%+ in the last few months, I am able to sleep at night - and continue to make purchases with my income in the bond market - to grow more income.

As for eliminating the taxable status of munis which has actually been discussed over many years (that’s not a new thing) but hasn’t come to fruition, we already know what this will look like. Why? Because taxable munis already exist.

For example, you can buy a Dallas Fort Worth Airport bond maturing in 2046. It’s interest rate is 2.843% taxable but it’s priced at $69.25 - with a yield to maturity of 5.24%. If called, you’d get $100 right away and a much higher yield.

There’s a Virginia Housing AA+ so bulletproof - 5.88% taxable with a yield to call of 5.72% taxable - so it sells at a slight premium - 101.

So if 4% tax free is the target, the taxable bonds equivalate to a tax free equivalent. A 5.72% in the 24% tax bracket is the equivalent of 4.35% tax free - and that’s worst case on that bond. If your state has an income tax, unless you are from the issue state, you’ll pay them too.

Microsoft stock is down from $468 to $388

AAPL from $260 to $198

ORCL from $198 to $132

TSLA from $488 to $252

UPS from $153 to $97

DIS from $118 to $84

BAC from $48 to $36

So yes, securities have fallen. I don’t know if MSFT, AAPL, ORCL, TSLA, UPs, DIS, or BAC will go up in price or continue to go down.

I do know that investment grade bonds most assuredly will pay $100 at maturity - regardless of the price today - and that allows one to sleep.

In essence, muni bonds continue to do what they’ve always done -they are drama free, a counter to equities (which I own too) but they’re the reason I can sleep at night.

And if tax free status is ever lost - and it’s been discussed for many many many years - no issue - because issuers will have to increase the yields - which is one of the reasons it’s never been pushed through (higher expense on the issuers).

It’s nice to put out FUD - Fear, Uncertainty and Doubt - but nothing about the benefits of munis has changed - they will still pay in full at maturity. The same cannot be assured for any stock or index.

People, of course, are free to invest as they seek fit - munis were pointed out simply as a way to assure income without the daily tumult of emotions caused by a volatile stock market. Volatility in bonds, when you own individual, is a zero issue.

1 Like

Great thing about long term investing is return results don’t lie. It’s a math problem.

It is universally acknowledged that for long term investors a balanced multi asset portfolio yields the greatest risk adjusted returns. The recent volatility highlights the pitfalls of single asset investing and the value of professional investment advice.

In spite of recent retrenchments here are the actual (as of today) 1 and 5 year price performances from some of the stocks mentioned.

Doesn’t take a quant to realize that having a portion of an investment portfolio in a few of these names or an equity index would have improved performance relative to a 4% municipal that underperformed as the Federal Reserve raised rates which in turn lowered the value of outstanding fixed income securities. While muni investors will get their principal back they haven’t kept up with inflation. Fixed income investors purchasing power is destroyed by the “double whammy” of rising interest rates and inflation.

Annual US Inflation rates

- 2020: 1.23%

- 2021: 4.70%

- 2022: 8.00%

- 2023: 4.11%

- 2024: 3.3%

In real terms the investor in an asset producing income of 4% was loosing money!!

Here are the actual results generated by the top two muni funds when using the market standard total return analysis.

The numbers are the numbers.

4 Likes

And this is why we have trust in our financial planner. He and his coworkers have looked at trends for many years.

I’m in a stay tuned mode.

6 Likes

Today we are experiencing a very uncommon and concerning phenomenon. US Treasury bond yields are rising significantly which in normalized markets very highly correlates to a stronger dollar. The dollar however is selling off versus all major currencies.

While the equity markets seem to want to prove resilient this UST and $ dynamic could prove much more significant to our real economy. This will quickly become the story I suspect.

4 Likes

Is that still happening? I haven’t paid too much attention. Ugh! I was hoping things were leveling off recently

10 year treasury is at a 4.40% yield and dollar vs BPST 1.32 and Euro 1.14.

Equity markets all now starting to soften off early open highs.

4 Likes

I think this is a wait and see mode for many of us. For those already retired, there are not years ahead for a recovery from market and bond losses.

If you are in your early 50’s, it’s my suggestion that you have a diverse retirement portfolio. You have more time to wait this out.

4 Likes

There’s no such thing - that’s what’s being missed - if you own individual bonds.

The only loss is if you paid a premium (over 100) but you would have known that when you bought the bond and it would have come with a commensurate yield for the premium. That’s the Virginia Housing bond I listed above at 101 but a 5.7% yield to call (meaning, if it’s paid off early, you still earned 5.7%).

Again, it’s a “ballast” if you will, an alternative to partially or for many wealthy - fully - provide a stress free income substitute. I don’t know about you but I’ve had times of market panic - I’m sure all have - so this is the part of the portfolio (not the entire) that allows one to sleep at night.

If there’s risk, it’s inflation risk - when I was earning 4% and inflation was higher, my real return was negative - but If one builds enough income (more than expenses), that matters little.

But bond market losses - impact you if you have a fund - but are not a thing when one holds individual issues. This is why the wealthy historically - from Ray Kroc (McDonalds) to Bill Gates to Linda McMahon (Education Secretary, whose filings show she earns $900K per year from muni bonds) - they pile in. Others include the Walton Family, Suze Orman. And so many wealthy (and non).

Buy what you want - but please don’t share that’s not pertinent to the long term capital preservation - as today’s bond price has zero relevance to the overall return of that security beyond the price and yield at the time of purchase, not the performance due to a rise or lowering of 10 year bond rates.

1 Like