In the years before college, if the family spends $40,000 of the remaining $133,000 on other things, then it would be saving $93,000 per year, and can effectively cash flow a $95,000 college bill in the years when that is present.

Of course, a lot of families get by on total pre-tax income much less than $133,000 per year.

I understand, and that is all reasonable math. But it is still side-stepping the underlying issue -

Do you think a family making $210k a year should pay a higher percentage of their annual income and assets for the same college than a family making $100-150K or a family making $500k+?

I know it seems like a problem with out a real victim, but schools are starting to recognize they are losing this cohort, and are doing some adjustments already (e.g. MIT increasing tuition-free aid packages up to $200K.

Let’s say one well known competitor made a move to add merit, then others might follow.

What would it take to happen?

They don’t get enough butts in seat. Maybe families don’t qualify for aid, but worry about the economy - so instead of going to Vassar, go to their state school. If enough of that happens.

F&M used to not give merit but changed. Why? I don’t know - but maybe because Lafayette, Dickinson, Gettysburg and other direct competitors do? Maybe they felt they were missing some of the target market?

It seems many schools are heading toward need vs. merit - is that for social purposes (they look better)?

Do market fluctuations cause them to reduce or for those on Questbridge, take less? Or are all these meet needs schools properly planned financially?

Only time will tell.

I’d imagine going to Need Aware from Need Blind might happen first…if anyone changed.

This. There has crept into the public discourse this idea that you’re supposed to be able to send your kids to college w/o skipping a beat. That was not the case when I was growing up, when the cost of education relative to real income (at least seemingly) was much more advantageous than it is today. It’s not a requirement to go to college. It’s also not a right. It’s something that has to be paid for. Private college? Yeah, if it’s a little beyond your means then it’s either save, do without a few things for a few years or don’t go. The idea that everyone is going to conclude “don’t go” is, I think, a little simplistic.

Also, I don’t think the threshold for the upper band used as a foundational predicate in this argument should be seven figures. People who make north of 250 and less than 1,000,000 commonly send their kids to the “best” school their kids get into and want to attend. They may skip a few things or defer some home projects, but if they care about it they’ll pay for it.

The super selectives have war chests that they are forever building on so that they can afford to educate whomever they choose, and the threshold for the “don’t worry; we’ll cover it” crowd seems to be increasing by the day. I’m always opening this and other sites surprised to read announcements like “Dartmouth to extend full financial aid support to families making less than … $[bigger number than I expected].”

As @NiceUnparticularMan once said to me when I asked, “why does Princeton need to worry about keeping their rich friends happy - aren’t they independent of all that now?”: They didn’t get that rich by resting on their laurels. They want to stay richer than everybody else and so they will always care about the big money class and fundraising.

That money is what will enable those schools, including LACs, to continue bringing in the kids they want by relying less and less on tuition.

There is always going to be an income / asset range that will feel this kind of resentment and grievance. Whatever level of income / assets that is where full pay list price begins will be paying a higher percentage than the plutocrat class, as well as likely a higher percentage than the top of the “no parent contribution” range if the college covers everything except for a small student work earnings amount. Note that the small student work earnings amount can be a much larger percentage of income an assets to very poor families than full pay list price is to the resentful upper middle class / semi-rich that you are referring to.

Again, I think this is intentionally creating a strawman and ignoring the actual argument. To try to eliminate the issue by painting it as “whiny rich people” totally misses the point.

In your opinion, should there be a specific income band that is required to pay a higher percentage of their income for colleges than other income bands? And if so, do you think that that band of people should be those making $200-$300k a year?

[And, to avoid the argument, obviously it shouldn’t be those making less than $100 either. I think to say lower-income people should bear the burden would be a ridiculous argument. But I do think there should be a difference between what someone making $200,001 pays for college and what someone making $1M a year pays. Under the current model there isn’t any difference at most schools]

I don’t buy the percentage argument. Nobody buys groceries with a percentage. Nobody pays their electric bill with a percentage. It’s just arithmetic that an increase in the cost of milk, eggs, whatever is going to hit the lower income family MUCH harder than that exact same increase for the 300k family. So no- the “greater percentage of income” for college argument doesn’t hold water for me. The higher income family STILL has MUCH more disposable income- to dispose of as they wish-- than the lower income family, despite being blessed by the financial aid fairies.

I think one of the issues is the creeping upwards of our standard of living- as a country. The notion that a family of four could live in the “Levittown” type house which was the norm after WW2-- no. Those houses required siblings to share a bedroom. That no longer flies unless you are poor or a member of a religious group where 5+ kids are the norm. Those houses had one bathroom- the fancy model also had a powder room. But families stood on line in the morning and that was the way it was. No garage- a carport. No A/C. And as I’ve learned in my own neighborhood when those “original” houses sell-- young couples are horrified that there is no great room/media room. The idea that everyone would congregate in the living room- no way. Dad needs a man cave, mom needs a she-shed, the kids divide up the great room/family room/crafts room.

So we’ve ratcheted up what a “normal” standard of living is. It costs more to build, to maintain, to repair. Each family member has a phone and in some homes, each family member has a big screen TV. Etc. Any wonder that collectively we’ve got to feel sorry for the $300K income family feeling stretched to send their kid to college?

I have great sympathy for anyone whose top priority is educating their kids and are finding that it requires enormous planning and self-restraint to make it happen. But I’m going to guess that there are dozens of posters on CC who’d be happy to help the 300K families do the planning and self-restraint so that their kids could get a great education.

At most schools, no they won’t. Or, the amount of need based aid won’t be nearly enough to make their overall payment less (percentage wise) than what high income families are paying.

Most schools don’t offer all that much financial aid…because they don’t have it to offer. Lots of low income students get Pell and Stafford (Federal money/Federal loans)…and that’s it. Then the families have to figure out how to come up with the rest of the money. Enter Parent Plus loans, private loans, extra hours at the job.

But that is how need-based aid is calculated. If percentage of available income and savings wasn’t taken into consideration, then people making $40K a year would pay full price. I assume you aren’t arguing for the elimination of all income based aid, just for those above a certain amount. You seem totally comfortable with that amount being somewhere in the $150 to $200 K range (where it currently is at most schools) and that is a fine opinion, but you must agree that for everyone under $200K need-based aid is in fact calculated based on what percentage of your available $ the college thinks you have available to pay for fees. It isn’t the same as eggs.

I don’t agree. Most school don’t bother to calculate. I’m assuming you have never seen a financial aid award from a “non-meets need” school (which is a large number of schools) handed to a middle income (well below 200K) earning family.

There is zero calculation of “percentage of income”. There is a line for the Pell Grant (a federal entitlement, so it’s not like it’s some gift from the college), any state funding available if you qualify, and the breakdown between your subsidized and non- subsidized loans. NOTHING to do with percentages, and nothing to do with availability of funds.

You are insisting that I should agree with you. You are describing a rarified set of circumstances and assuming it is the norm. It is not. Have you ever wondered why a significant percentage of kids in America attend college within commuting distance of their home, and attend a public institution? No, it’s not because they can’t leave Mommy and Daddy. It’s because that it is the ONLY affordable option to getting a Bachelor’s degree.

If you make $300k in W2 salary, after all federal and state taxes you take home about $189,000.

NPC results for the proposed scenario of $300k - $100k fed taxes, with no savings, investment or similar assets is below and a 14-year-old younger sibling. In the unlikely scenario where a person with <$200k after tax income has 0 assets, they aren’t expected to pay anything close to $95k/year at the listed colleges.

Georgetown – $42k/year

Tufts – $41k/year

Dartmouth – $28k/year

A summary of how the Dartmouth numbers change, as I change settings is below. I expect most persons with $300k AGI have less than 33% fed tax rate after deductions, and have significant savings and investments. With these changes, prices get much higher, with a large portion being full pay. However, having more after tax income and more savings also means the college is likely to be affordable.

Yes, that $300K income with absolutely no assets is indeed an incredibly unlikely scenario. Under almost any real world scenario, people making $300k and having assets do not get any aid. I don’t think that is a controversial statement.

It seems that many of those vocal in this thread are totally fine with the status quo and think that those in the “middle-high” income group are simply entitled whiners. That is a totally fine opinion to have.

It does however genuinely impact real people and quite a few colleges are noticing that they are losing this cohort and are starting to change their aid calculation to get them back. In the meantime, real kids like the examples I gave above are not applying to schools for which they would otherwise be a great fit.

I am NOT totally fine with the status quo. The reality that a school librarian who moonlights at night as a tutor and works all summer running programs at the YMCA camp discovers that she cannot afford to send her HS kid to the state flagship- no, I’m not OK with that.

That’s the status quo that many of us here are upset about- that social workers and teachers and police officers and nurses discover that they are in a different donut hole than the one you describe. They are in the “send your kid to community college and they can get a certificate in phlebotomy” donut hole because our public institutions have priced themselves beyond the capacity of many wage earners in the state. We’re talking tax paying citizens.

I applaud you thinking of alternative ways to make sure that every capable kid in America who wants to go to college can get there. But focusing on the $300K crowd is not likely a popular cause right now. Those kids usually have had every advantage growing up, and their families have the financial wherewithal to figure out how to finance college.

As stated in my earlier post, it depends on how large the assets are. For example, having $200K in cash savings had little impact on cost at Dartmouth, while having $400k savings + $1M investments nearly brought the cost to full pay. The expectation is that the $300k/year income family with $1.4M in non-retirement savings/investment assets is expected to contribute a portion of those assets to the college cost and/or cut back on their lifestyle expenses while their kid is in college.

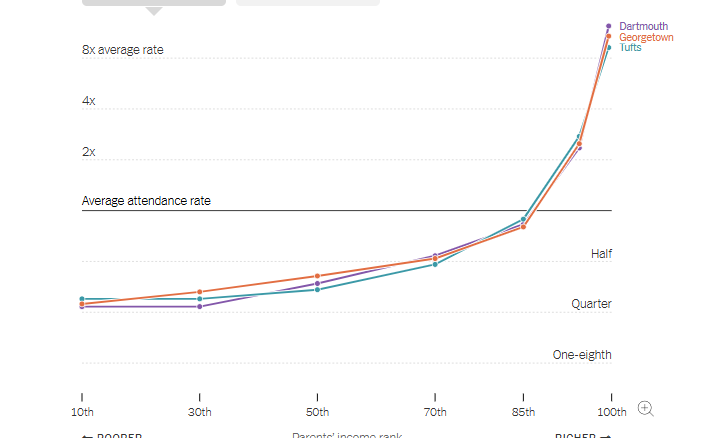

What is far less controversial is that the $300k income families are not an unrepresented donut hole at the listed colleges. $300k income corresponds to ~95th percentile. 95th percentile is one of the points appearing in the earlier Chetty graphs. A graph for the 3 previously listed colleges is below. All 3 look nearly identical, with a 3x overrepresentation among 95th percentile families. There is nothing to suggest that the FA sliding scale is causing $300k/year families to avoid the college more than lower/middle income families that typically have less assets, and receive greater FA.

I’d guess that these schools would be entirely populated by kids from umc/wealthy families instead of being mainly populated by kids from umc/wealthy families.

well that “95%-100%” includes people making anywhere from $300k up to $5M+ though. So it hardly contains the granularity to tease out the decisions being made by actual families making $300K. Again, based on anecdotal evidence, the majority in that group are sending their kids to publics or to schools providing merit, not paying full cost at privates.

Also, as a separate but important point, regardless of how much a percentage of your income it represents, it is very hard to justify paying $90k a year for an undergraduate education from an ROI standpoint. If you make $2M a year and don’t care much about ROI then that is one thing, but for everyone else, the difference in ROI between a school costing $60k and $90K would not justify a $120K difference in cost.

Believe it or not, there are folks at all income levels who do not believe that they can accurately predict the ROI for their 17 year old kid. They don’t try.

They know that the labor markets are hard to predict, are sometimes capricious, are often a lag on key economic indicators, and at other times, are the proverbial “canary in the coal mine”. They’ve seen kids majoring in Petroleum Engineering which is a rock solid, high paying career except in the years where Big Energy stops hiring altogether. They’ve seen kids majoring in Finance graduating into recessions (remember the class of 2009?) where there are no jobs, and they remember when math majors were driving taxis and software engineers were working as substitute teachers in middle school because it was the ONLY job they could get.

So I admire your confidence that you think people are crunching the numbers and making decisions based on the ROI some years hence- and out into the future for the 40+ years of wage earning. And that they’ll be right most of the time. Most people can barely fill out their own tax returns, let alone conduct a sensitivity analysis on the payout of their kid’s college experience.