I think that QB will definitely say that there are no hard cutoffs. I also think that it is unlikely that the OP would qualify financially for the college prep program and be disqualified for financial reasons from the match program. While I know that not all college prep scholars are admitted to the match program, I think they are trying to capture the same demographic.

1 Like

There’s no ‘disqualification’ process/option of applications submitted to the National College Match (assuming a completed app.) The issue is whether or not the asset is a material factor in becoming a finalist. IMO it’s likely a factor, but maybe not as a large as grades/rigor/test score. I’m not sure, and I doubt a QB rep would/could say with any certainty either.

My advice to the OP is similar to some other posters. If you want to attend a residential college with the full COA covered, I think that you should reconsider your QB list rather than only applying to the ones with the biggest names.

Also, I would consider applying to be a gates scholar. If you are eligible for a pell grant, you are eligible for that scholarship. The whole process is grueling but the first round application is easy so there is no reason not throw in an application. It is only the later rounds that require essays. While my daughters did not apply to QB (eldest was told that she’d be unlikely to be admitted), they both eventually won Gates and a couple other national scholarships. The conventional wisdom on CC is not to try for those programs, but they do work out for some students and there is a lot of cross-over between QB finalists and Gates scholars. Furthermore if you win one of the national ones then you can take it to any college that admits you so if you are not matched, you can use it at Rutgers or anywhere.

8 Likes

Note that most of these (except Chicago) do require the non-custodial parent waiver. This adds another possible way to be (effectively) rejected.

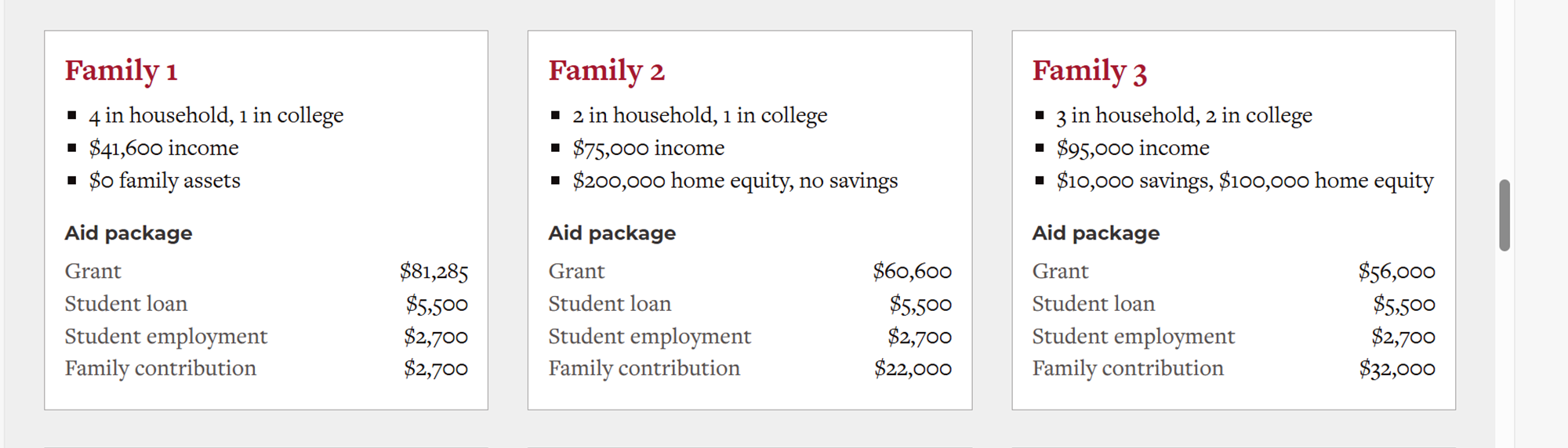

Good catch on Lafayette. I just “googled” and what I used was College Raptor…ugh! Sorry. I just re ran - results below.

The Oberlin examples came from their website - they put 7 or 8 scenarios. I didn’t run NPCs.

#2 was the “closest” example but OP has less salary, more home. I put below too.

There was an article about Lafayette a few years ago - showing how need aware works. Maybe it’s different now - but they’d turn a student like this down - based on the amount of need. I linked that below as well. It’s quite interesting.

Thanks for second guessing me.

OP - Was the house reported to the Prep Scholars program last year?

Given what the OP has told us, the non-custodial parent waiver seems like a very easy next step. No contact, the school system will not allow the NCP access to the kid, zero paid in child support or- presumably- alimony. Seems like a textbook definition and exactly why the waivers were created.

5 Likes

Just as a note— OP is a family of two, not four.

And I think they said that the duplex was from money that other family members pooled to make it possible.

OP— if the latter is correct you may want to try to find out if your mom is the only person on the deed or if your half of the duplex is actually a shared ownership. That might be important for QB financial qualification.

2 Likes

OP— if you use the site blockshopper.com it usually lists the current owners of an addeess

Hello everyone. I just emailed every single QB partner and QuestBridge themselves about whether primary home equity is factored into financial aid.

It took me about 2 hours to do all this, but I hope future students can use it as a resource! Here’s what I found, paired with some of my own research & NPC tests:

![]() EXCLUDES primary home equity completely

EXCLUDES primary home equity completely

- Brown University

- California Institute of Technology

- Colorado College

- Denison University

- Harvard College

- Massachusetts Institute of Technology

- Princeton University

- Stanford University

- University of Chicago

- University of Notre Dame

- University of Pennsylvania

- University of Southern California

- University of Virginia

- Washington University in St. Louis

![]() CAPS primary home equity at X times parent income

CAPS primary home equity at X times parent income

- Amherst College: caps at ~1.2–2.4× income

- Boston University: caps at 2.5× income

- Colgate University: caps at 2× income

- Columbia University: caps at 2.5× income (per NPC)

- Cornell University: caps at 1.2× income

- Dartmouth College: caps at 1.2× income

- Davidson College: caps at 2× income

- Duke University: per NPC appears to cap at ~1× income

- Grinnell College: caps at 2× income

- Johns Hopkins University: caps at 1× income

- Oberlin College: caps at 2× income

- Rice University: caps at 2× income

- Scripps College: caps at 2.4× income

- Skidmore College: caps at 3× income

- Tufts University: caps at 2× income

- University of Richmond: caps at 2× income

- Vanderbilt University: caps at 2.4× income

- Vassar College: caps at 2× income

- Washington and Lee University: cap varies, case by case

- Williams College: caps at 1.2× income

![]() INCLUDES full primary home equity in calculation

INCLUDES full primary home equity in calculation

- Bates College

- Boston College

- Bowdoin College

- Carleton College

- Case Western Reserve University

- Claremont McKenna College

- Colby College (but possible appeal to remove)

- College of the Holy Cross

- Emory University

- Hamilton College

- Haverford College

- Macalester College

- Middlebury College

- Northwestern University

- Pomona College

- Smith College

- Swarthmore College

- Wellesley College

- Wesleyan University

- Yale University

Interestingly, a Boston College FinAid rep told me:

“If you live in a duplex split 50/50 (with separate entrances), you would need to report half of that $450,000 value ($225,000) as a real estate asset on the FAFSA if the form asks about family assets.”

Took a long time but worth it! Waiting on a response from Questbridge, but I expect them to not give me a substantive answer lol

8 Likes

Thank you for this. Will look into the Gates Scholarship, was also looking at a few other ones as well. Going to apply broadly with regards to scholarship to maximize my chances.

Yes, the latter is correct, going to inquire if its a shared ownership

It sounds like they misunderstood. Either that or I did. My impression was that YOUR unit in this house was valued at $450,000….not the whole house. If that is the case, the whole amount would be used. You don’t even own the other half of the house, right?

2 Likes

Yes, our address which is our unit is valued at 450k. Looks like they misunderstood. We dont own the other half of the house, it was bought in 1999 whereas ours was purchased in 2023 when I moved from Chicago

2 Likes

Question I asked earlier - when you were in the prep program - did you report the house?

Since it just came up yesterday, I’m guessing not.

I ask because some have suggested the targets for the Prep and Match program are the same - but they might not have been given the same info.

Also, all the NCPs ask if mom has any money in the bank. I’m guessing not a lot but there has to be some - $1,000 or $5,000. I don’t think any of us included that - but that might throw things off a hair too.

Thanks

Yes, QB asks for assets but that is the only asset that I had to report( my primary residence). My mom does not have much money in the bank. 1k-5k is a fair range. I emailed every QB school yesterday like you asked me to, did additional research, and ran NPCs for most of them. The issue is that the ones that exlude primary home equity would be reaches for me, correct?

All schools with sub 20% admit rates are reaches for you. Some schools with admit rates in the low 20%’s are likely reaches too. It’s difficult to parse different degrees of reachiness.

4 Likes

But then again with sub 20% acceptance rate schools, those are reaches for everybody. Never know if you dont apply.

1 Like

I agree (for the vast majority of applicants.)

The question is how many reaches are you going to apply to and write supplements for? QB 15 schools and another 5 reaches puts you at 20. It’s hard to do that many supplements well.

2 Likes

Every QB school is a reach as I said earlier.

But the ones that show a contribution for you - and QB is a full ride - well my guess is - you have too much $$ for them. They are looking for people worse off financially I’d assume given the ethos of the program.

Hence you’d be smartest to apply to the NPCs that have the lowest out of pocket - which likely line up with those that don’t count home equity.

But make no mistake - while I hope you get matched and if QB says you will not be excluded and you apply - I wouldn’t expect it.

That’s just being honest as I was all along - but again, I’m not an adcom and not a QB adcom (that’s just my guess) - and all 55s schools on that list will have people at Rutgers, who chose Rutgers over those schools. Yep, people choose Rutgers (and far less prestigious schools) over the Ivys.

Your SAT is great but your STEM results are a concern (to me)…

As it turns out, those who apply have a chance to get in.

Those who don’t - don’t have a chance.

So you take your chance, do your best, and hope.

Stop worrying about what people think your odds are. You want this - so do this (assuming QB blesses the house not an issue).

If they say it is, then you can still apply - but outside the program.

It’s interesting to me you say you reported the house last year to them…as it just popped up yesterday.

But if you did last year and told them you had a $400K asset and they still enrolled you, that’s a good sign for your continuance I’d say.

1 Like