Good! He can lead by example and transfer a billion dollars to the SS fund. In fact, anyone with a net worth of over 1 billion should be made to transfer that amount to the fund. All our financial problems will disappear!

6 Likes

According to Wikipedia there are 756 billionaires in the US. If we took one billion dollars from each of them that would buy us just a few more years before needing to do even more.

3 Likes

He’s still working at 71.

I’m not sure why eliminating the income cutoff for contributions doesn’t get more traction. It must not be popular with lawmakers and their donors. It is a solution favored by a majority of Americans. Even if it was a reduced percentage on higher income.

7 Likes

I have no doubt that will be part of the solution, when a solution actually gets discussed.

But the reason for the income cap is that there was a fear by Ted Kennedy and others if the cap was raised any higher, than SS would no longer be perceived as “old age insurance” but a welfare program. The fear was that a welfare program would be easier to reduce. (Since benefits are capped, higher contributions by the higher income would result in no additional benefit to them. )

Yeah, I get that most won’t cry a tear for higher income folks, but just sharing what was a concern years ago.

Please do not stray into politics!

3 Likes

I meant take away all the money over $1B. ![]()

Yes, that wouldn’t cause any economic issues whatsoever to suddenly confiscate the net worth of those individuals. And, I doubt it would make retirement any easier for anyone else.

3 Likes

The reason no one in charge wants to eliminate the income cutoff for SS contributions isn’t because they care about the worker making $300-400K. Most of the decision makers could careless about people at that income level. The reason it doesn’t get done is because the corporations would also have to fund the employer portion (6.2%) along with the worker. And we all know just how much employers/corporations are willing to pay taxes.

For example the NBA Salary Cap is $141M. A team pays 13-14 players who will all max out at $168K for SS. That would leave roughly $138.5M in wages not subject to SS. For the team/employer if there wasn’t a max on SS then the team would have to contribute $8-9M more to SS. Those billionaire owners are not going to take that hit and they are going to lobby their friends in D.C. to make sure that never happens.

One day we will all wake up and realize there are tons more regular people than there are rich people. And when I say rich people I mainly am talking about billionaires. Because you have to realize that if your net worth is say $4M you are way closer to the homeless guy on the corner than you will ever be to people like Buffet, Gates, Cuban or Bezos.

7 Likes

You are over-simplifying this issue. Ultra-high earners have plenty of ways to avoid income being wage income subject to social security. They make much of their income though capital gains. And high earnings can be structured as profits (eg in an S Corp or partnership) or dividends to avoid paying social security on them. Billionaires like Zuckerberg don’t even take a salary from their company (and can borrow against their shares to avoid even paying capital gains taxes). That’s why some politicians talk about taxing unrealized capital gains (though that would be very challenging to implement). So the burden would fall on wage earners making $300K-$400K who don’t have sufficient control over their company’s structure to engage in these maneuvers.

2 Likes

They wouldn’t end up taking a hit in the end, they’d just pass that cost along to ticket purchasers, etc. Same with other businesses, the cost would be passed along. Of course, I’m sure there are some big lobbys against it. In the end, to me anyway, it seems like a more reasonable way to ensure the solvency of Social Security.

1 Like

Getting a bit off topic. How SS will impact on your own retirement and have an impact (or not) on when you/spouse retire.

1 Like

I think you are not seeing my point.

I am not talking about Zuckerberg’s personal taxes for himself. I am talking about the employer portion of SS. Meta has a ton of employees that will go over the SS cap. If SS was uncapped like medicare then Meta itself would also have to kick in/pay 6.2% of the salary above the cap.

Just in case you don’t realize when 6.2% is withheld from your check your employer also pays in 6.2% for SS.

Think about all the tech workers that are earning more than $168K.

4 Likes

I don’t really understand why people say that we have not have paid fully for our social security benefits. For example, I paid into social security for 43 years, most of those years at the max. If I had invested those contributions at just a 4% return, the amount would be well over a million when I start collecting, in fact the monthly payment wouldn’t touch the principal. That doesn’t even include my employers contributions. If I consider getting a 0% return for both my employers contributions and mine, it’s still over 600K. How is that not easily paying for itself? And I could end up collecting nothing.

Unless, of course, it’s because what I paid in has nothing to do with the actual cost, and that it’s really just another tax that pays for whatever. If they want people to pay even more for their social security and collect less, at least be honest about it being a welfare program.

But social security is critical to most people’s retirement stability. So many people go through their savings and have nothing else.

4 Likes

My point is exactly that, it’s the tech workers and other salaried employees making a few hundred thousand a year that will be affected. But previously you said

And also gave an example of a few hundred basketball players making millions a year.

The employer contribution issue is a red herring. Most companies don’t have huge numbers of employees making more than $168K, and the share of payroll that would be newly subject to payroll tax is very limited. A few companies like in tech have very high earning employees, but most of that is share based compensation where the company gets to deduct that share compensation from corporate taxable income even though they didn’t spend any cash to give those shares out. They don’t care that much (and if they did they’d just give out fewer shares), just like the tax rules that prevent deductIon of CEO salaries of more than $1M don’t stop CEOs getting paid a lot more than $1M.

Or they never made enough money to have significant savings and do not have a pension. I know at least one person in that situation.

8 Likes

This came up in my workplace yesterday. A co-worker was talking to a retired co-worker. The retiree needed to contact our HR because after this year, they won’t have to file federal taxes. I was shocked. How? My co-worker said that once you get to be a certain age, you don’t have to file taxes any more. Her parents haven’t filed for years. I was scratching my head because I’m pretty certain my parents still do. I read it’s not age based, it’s income based. If you make < standard deductions, you don’t have to file. So my co-workers parents and my former coworker (who does get a pension from my workplace) both fall into that category. I can assure you that neither have significant assets either. For most of the retiree’s employment, they made < $30K and are single.

I also looked at our retirement information: only 20% of our retiree’s pensions are > $2000/month, and I would guess most of these belong to former police and fire. Their pensions are significantly higher because they don’t get SS. 27% of our retirees have a pension < $1000/month.

So yes, SS is VERY important to a lot of people around here. It will be important to me/H, but we could get by with a reduced amount.

10 Likes

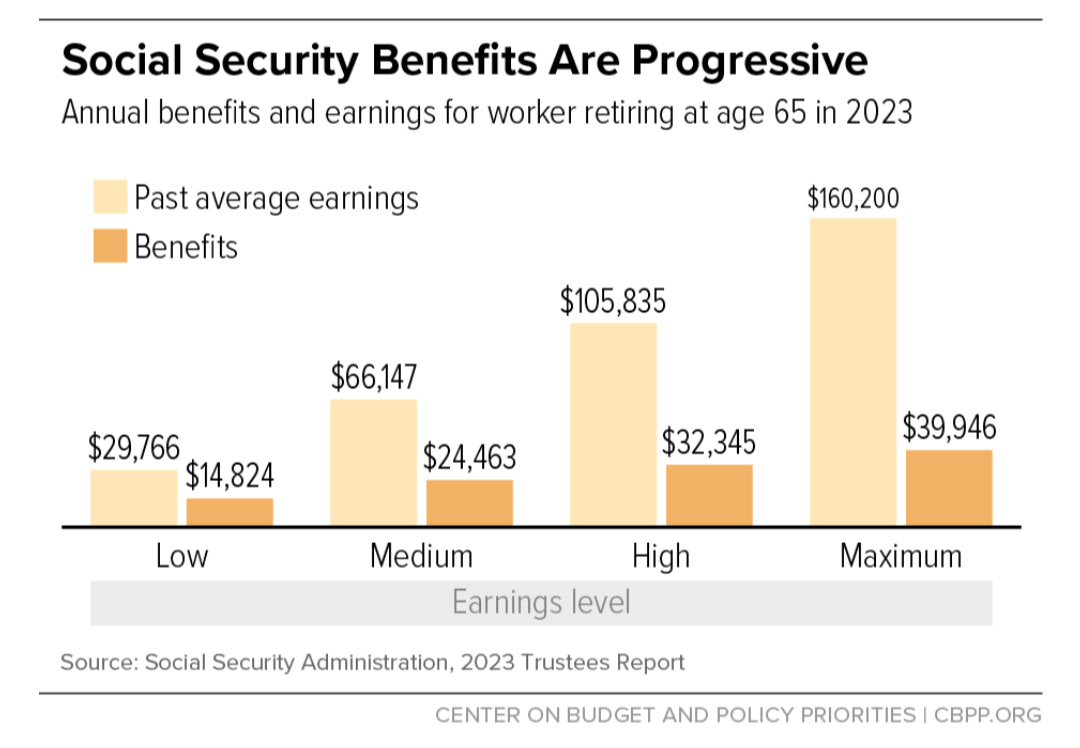

The fact is the vast majority are not paying in as much as you and many will collect more than they personally paid in comparably. It’s a progressive payout as seen below.

3 Likes

Yes, Social Security is absolutely important to many. My parents relied exclusively on it and after seeing how minimally that money provided for retirement needs I knew I had to do something to supplement it. In the end, it wasn’t meant to pay for 100%of ones retirement needs. Hopefully we can do something to keep those benefits flowing.

6 Likes

SS is a regressive tax/payout…. that’s OK with me. More thoughts from an editorial (I agree with some, not all) Social Security was always intended to be a regressive tax (6.2% | by Opher Ganel | Medium

1 Like