That seems like an incredible deal unless the base price is sky high.

1 Like

The buy-in is quite high, at least for us.

1 Like

My MIL turns 100 this month! She lives in an expensive independent living high rise and has been there since shortly after my FIL passed away. He was cheap and never wanted to move there, while my MIL tried for years to talk him into it.

She had money from her first husband and worked until she was about 60. While she has long term insurance, she has never needed it; she is very active and healthy. As her investments have done well, she has been able to live off her interest and not sure she has touched her original investments. While I would love to be able to do the same, I do worry about the money I have lasting me for possibly 30+ years as I do not have long term care insurance. While I do not want to live to 100, I would like to not be a burden on my children.

5 Likes

It can’t hurt to do some early research. We have sometimes dropped into real estate open houses just for kicks (and to check out their decor, renovation ideas). Our observation is “looking at houses is a lot more fun when you are NOT in the market”.

4 Likes

Is there any provision for folks to get partial refund if they later opt to move closer to family?

There are three levels of buy-in – nonrefundable, 50% refundable and 90% refundable. Of course, the refundable options are a higher buy-in. And even the nonrefundable is partially refundable until you are there 50 months. So, if after three months you realize this isn’t the place for you, they will charge you 2%/month and give you back the rest.

3 Likes

My mother in law had about 4.5 million in assets she started needing round the clock care. Because her assets were generating around 5 percent a year or more some years in income off that amount and the tax benefits of high medical costs meant that when she died 6 years later she had around…. 4.5 million.

5 Likes

Shouldn’t 2.7 million be generating at least 50 k a year income? ( that less than about 2.5 percent on his assets).

Another thing to keep in mind about Medicare is that your premiums are higher as your income increases. We found out the hard way: we did some Roth conversations that raised our premiums.

3 Likes

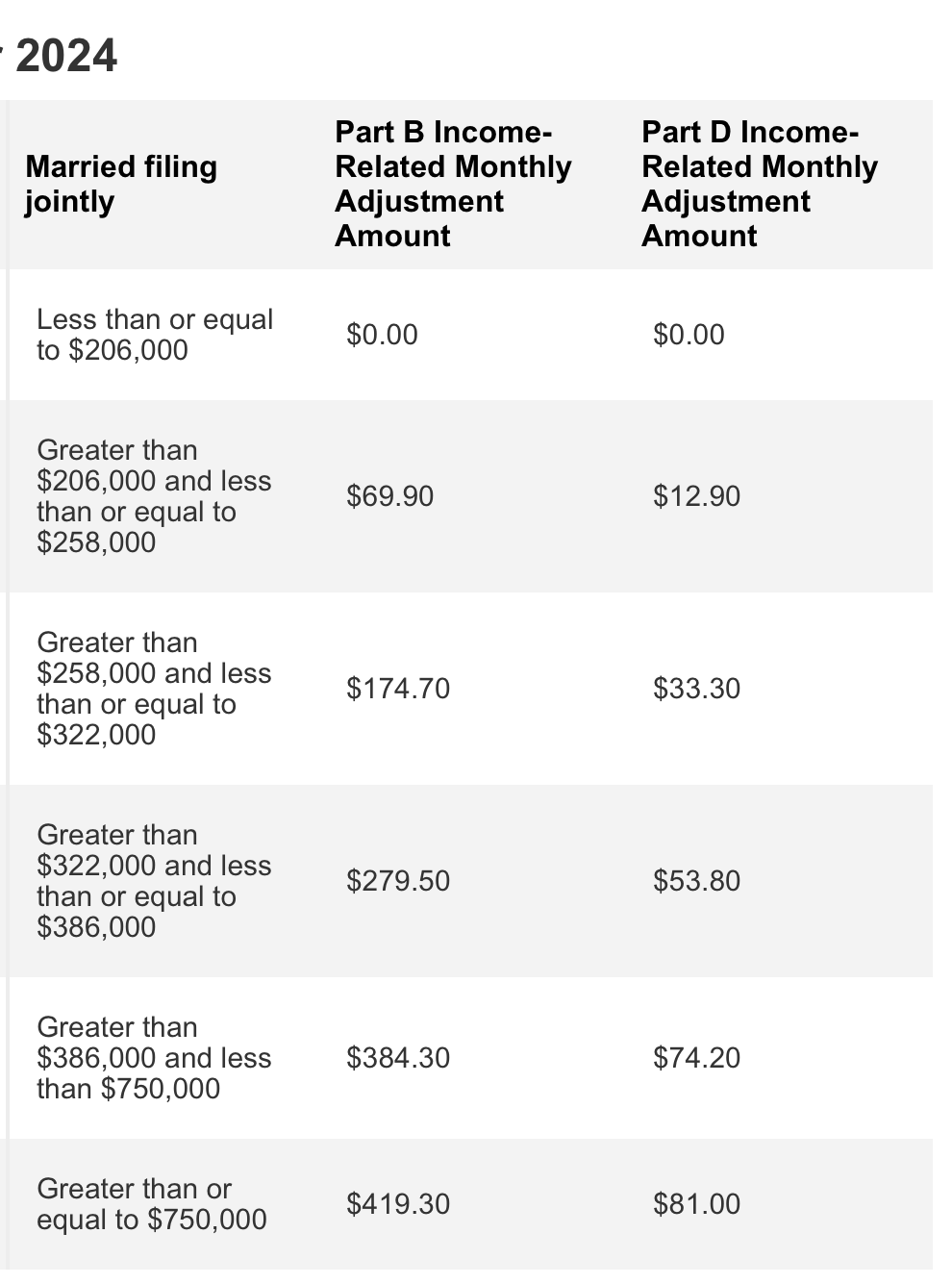

The above link has very helpful charts showing total costs at different income levels. But if a married couple keeps total income (incl investment earnings, capital gains, Roth rollovers) under $206K, no IRMAA concerns.

Showing it a different way, here is the “Adjustment” (penalty) chart (x2 if both spouses age 65+):

chart from Medicare Premiums 2024: IRMAA for Parts B and D | Kiplinger

1 Like

The 2.7 million was a cost figure I got by multiplying his current costs for 15 years per cbreeze’s question, not the amount of his assets. It’s not likely that someone would be in AL for that long. Most people die within 2 years of entering AL but there are always outliers. I think that people who have longevity running in their family need to possibly overestimate how much they will need.

2 Likes

I have never heard this. That seems way too short to me. My father spent several years in AL, including over 2 years of pandemic, and has now spent almost 2 years in a nursing home. I don’t think he is that much of an outlier.

I imagine it is hard to compile data for length of stay. Here is one source I found….

from https://health.usnews.com/best-nursing-homes/articles/nursing-home-facts-and-statistics - ## How Long Is the Average Stay in a Nursing Home?

Because of the wide variability of care needs across such a diverse population, it can be difficult to determine how long you’ll need care in a nursing home. However, the Administration on Aging reports that women on average need long-term care services and support for 3.7 years, while men average 2.2. years. About 20% of people age 65 will need long-term care support for longer than five years, the AOA notes. Approximately one-third of people the same age won’t need support at all.

Those figures include all kinds of long-term care, including assisted living communities. For nursing homes specifically, the average stay is one year, and about 35% of people use that type of care, according to the AOA.

3 Likes

I believe the average may be dropping a bit - I recall about 20 years ago the average time in AL was about 3 years. Maybe not death but going onto skilled care.

Maybe people are going to IL, AL, skilled care all under one system care - so they begin in their own apartment until needing AL or skilled care.

Some people absolutely ignore what they can handle staying in their own home, until something catastrophic happens or they have a hospitalization, and it is unsafe for them to return home.

Our home is not only getting a facelift, but DD1 was home briefly (flew in for a funeral) and went through the boxes and hanging girls’ clothing we had here stored in our generous storage area - what she wants and what we should donate. DD1 has two daughters (along with two sons) and a baby due in March 2025. Keeping about half what was in the boxes, and almost all of what was hanging up, including mother/daughter matching dresses.

My next step will be go through the stored toy area - which we have been gleaning some of that already. She wants the wooden puzzles and I am having trouble locating that. Tells you how much stuff I have here to go through.

2 Likes

You are probably right. Now that there more options for Independent Living and in home health care, the need for Assisted Living / Nursing home can be deferred. Of course there may still be increased expenses in those prior stages.

Good for you both to be privy to their information, as they need to have caring people watch out for them and their finances.

Their medical needs may eat up some of their estate, but being careful on their health and well-being is definitely good for all.

DH and his brothers were fortunate to have the parents’ home free and clear, and a bit of some small assets left from savings account and mom’s teacher retirement account and insurance. Homeowner’s insurance and taxes are not very expensive, and the family is hanging onto the home for a while - granddaughter most likely will become the final owner at some future date (her dad is the one who lives closest to the home, and he keeps everything up along with some hired help and watchful neighbors) - neighbors benefit from use of the carport and garage at no charge.

My parents did not have strung out medical or long-term care expenses. Dad had aggressive cancer and only a few extra days in hospital hospice after a dramatic decline in his last week in the hospital. Mom had dementia which she was able to mask for a while, but then she would forget to eat or how to put a sandwich together (would eat what was put down in front of her, as she was hungry); brother hired live in housekeeper/cook and he lived a house away - mom was a calm/non-combative and wanted to die in her home so she was quite content knowing she didn’t have to worry about anything and had a small companion dog (something she did not have before dementia became apparent) which was a good thing for her. With five of us siblings, we all received a fair amount of cash (lower six figures each) in 2011 after mother’s death – which went a whole lot further in 2011 than it does now…

Long-term care insurance is not a blanket insurance that is ‘all protective’ - carefully spelled out when insurance will kick in and also how it will and will not pay out. For example, it won’t pay for related people doing care – so have to pay an agency if living at one’s home and they qualify for insurance payout. Activities of Daily Living - that is spelled out on how much the person is disabled. Dementia throws one into qualifying for payout.

Being ‘self-insured’ for care often works out well for many - the insurance premiums might end up being a sunk cost versus investments with the money.

My point was that in determining how much you need, you have to account for some growth in assets. So if one has 2 plus million in assets, even in very conservative growth, the 2.7 will be unlikely to be depleted at all based on a 50K “shortfall” from SS and pension income. The “shortfall” would be made up from investment income (which gets a tax break based on the high level of medical expense)

3 Likes

It’s always hard to believe that one is an “outlier”. But yes…for MOST people ( which only means more than half…not all) the stay is not that long.

1 Like

I wonder if this is because so many old people resist leaving their home. They end up moving only when their health is so poor they can’t possibly stay at home. I have a friend with 95 old parents who refuse to leave their home. They really need the round the clock care of a nursing home (have needed this for at least the past 5 years).

2 Likes

I asked NJSue about her father’s expenses specifically because she mentioned his high medical costs, which could affect his assets. I was looking for a rough estimate of those expenses, rather than details on how he’s covering them. As we all know, Social Security alone isn’t enough to cover living costs, making investment income crucial. Sadly, many people in the U.S. don’t have that option.